“Davidson” Submits:

One might think that with the thousands of very bright people, 100s of thousands of MBA decreed over the decades and the number of Nobel Prizes conferred that someone somewhere would have by this time identified what is the “Fair Market Price” of investment markets. The facts revealed by historical study reveal that many opinions are present at all points during an investment cycle and that many accept the concepts of “The Invisible Hand” and “The Efficient Market Theory”. Each in its own way declares that “Fair” market prices are established by the confluence of buyers and sellers in the prices which we see every day.

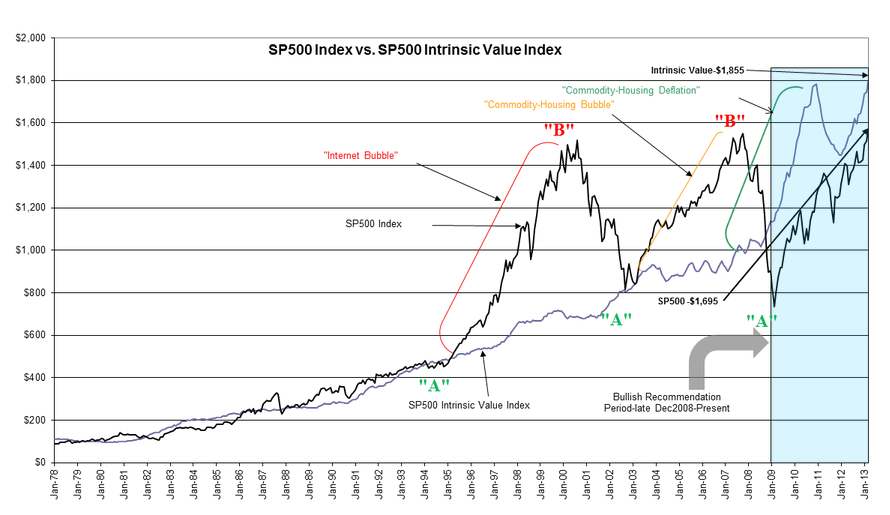

For those of you who have received my notes for some time, you know that I disagree with the concept of markets setting prices at “fair” levels. Markets are human systems! Human systems invariably imply higher social value to some items over others and general social consensus confirms this to be true. In the financial markets securities can be priced well away from their measurable long term returns and often are, due to “Market Psychology”. We have actually seen this fairly frequently since 1995 since Hedge Funds emerged to become a significant influence of market prices. In the chart below, SP500 Index ($SPY) vs. SP500 Intrinsic Value Index, I show the SP500 against an index which I created which I think provides a reasonable measure of market “fair” pricing which I call the SP500 Intrinsic Value Index. Think of this index as representing the market’s “Fair Price” vs. “Market Psychology” Prices which are represented by the SP500. This benchmark comes from the “Prevailing Rate”

Since 1995, Hedge Funds have become a dominant influence in market pricing. We know this by reading the literature. We have also have had one investment “Bubble” after another with the Internet Bubble in 2000, the Housing Bubble ($XHB) in 2005-6, the Peak Oil Bubble in 2007-8 ($USO), the Fear of Inflation and Collapse of the US$ Bubble in 2011 (Gold ($GLD) peaked $1,867.60 Sept 9, 2011), Fear of Euro Collapse 2012(10yr Treas Rates bottomed 1.394% July 2012) and there have been mini-“bubbles” as cash has rapidly shifted from one situation to another. This type of behavior is actually not different from the past, but it is occurring much more quickly. Along the way any sense of “fair” pricing of tends to evaporate as investors seek to avoid losses and reap gains by following what “the market thinks”. Those who believe that the “market knows all” and chase each trend include most of those people on CNBC with “something significant to say” to say every day.

Prices often do not represent the business returns of the underlying businesses. Take Tesla ($TSLA) for example. Tesla is currently priced at ~$15bil, but has less than $1bil of Revenue (a Price to Sales factor of ~15) and the TTM (Trailing 12mos) Earnings Per Share is reported as a loss of ~$2.70/shr for investors. This investment is trading very much like the Internet stocks of the late 1990s. Tesla does not have as yet a business return one can measure with which to predict if today’s price is worth buying in comparison to all of the opportunities available. This is a news driven investment as Tesla has had quite of bit of press with Founder/CEO Elon Musk being very smart and always in the news. I have no idea if Tesla will eventually prove to be an investment which actually trades on a measurable business return, but history indicates that it will, eventually. When it does, it will have to do much better than Ford ($F) which sells at ~0.5 x Revenue of $130bil and Toyota ($TM) which sells at ~0.9 x Revenue of $220bil. Ford and Toyota have measurable business returns and are deemed, considering how they are currently managed, to be very good companies. My net/net is that Tesla even with the brilliance of Musk looks to be in a significant “bubble” to me. These types of events occur primarily because, in my observation, investors do not have a historical pricing benchmark and assume that the market’s “Invisible Hand” provides “fair” pricing. What is actually happening is that investors are amplifying each other’s investment activity. Believing that some one knows more than they do, these investors pile into the trend of the moment driving prices to an extreme. There is a term given to these types of investors which many wear proudly; they are called Momentum Investors. (I do not recommend any of the companies discussed.)

To counter this one begins by constructing a valuation benchmark using economics. The difficulty is developing a benchmark is that economic conditions vary across the business cycle and even across wide swaths of our economic history. But, with study, one can come to the conclusion that in order for stocks to even exist, they must provide a return higher than the general economy or otherwise investors would not have interest. This means that the US long term GDP has the means to be our valuation benchmark. If the measurable returns of one company are significantly better than the general economy and other companies over time, then the stock of this company should sell significantly higher than other stocks and in proportion to its excess performance vs. GDP. It turns out that when one does all the work, of the components of GDP, Real GDP has long term predictability while inflation does not. What one does then is to use the long term trend (~25yr trend RGDP) of Real GDP and add back into it the best measure of inflation on a 12mo basis one can identify. This is where the “Prevailing Rate” comes from.

The “Prevailing Rate” is used to capitalize the reported Net Income of the SP500. But, I do not use today’s reported numbers which are high relative to the longer term mean, I actually use the SP500 Mean Earnings. The reason for doing this came to me a number of years ago as I was reading the various announcements of known Value Investors buying into severe market downturns. Warren Buffett and other true Value Investors when they make an investment are buying an earnings stream which is at least 5yrs-10yrs in the future. Good Value Investors are buying stocks for their representative company’s future earnings. They are NOT buying these issues based on currently reported earnings disasters.

Value Investors are disciplined buyers of business returns. They price a company based on its long term earnings stream using the context of the expected GDP trend. The “Prevailing Rate” represents that context as best I think it can be estimated. The SP500 Long Term Mean Earnings are capitalized (read this as – “divided by”) to give the SP500 Intrinsic Value Index at any point in time. It is the level of the SP500 Intrinsic Value Index which shows the price of the SP500 which represents the level most attractive to Value Investors. I use is as the “fair” value of the market within the context of the longer term economic climate. High inflation increases the “Prevailing Rate” justifying lower stock prices while low inflation reduces the “Prevailing Rate” and justifies higher stock prices.

Back to the chart! The SP500 Intrinsic Value Index as shown by the GRAY BLUE LINE represents my observations that Value Investor buying results in major stock market bottoms. When the SP500 is near or below the SP500 Intrinsic Value Index, investors will find that business returns are priced attractively in stocks for the long run. The higher the SP500 moves above the SP500 Intrinsic Value Index, the less attractive stocks become vs. their long term earnings trend. We have seen excesses in all markets at times, but since 1995 with the emergence of Hedge Funds we have experienced over and underpricing at extreme levels not seen since 1978. My guess is that we will see overpricing once again and it may be as high as we have experienced in the recent past. I expect to take advantage of this overpricing when it occurs.

Today, the SP500 remains cheaper than the SP500 Intrinsic Value Index. Today the SP500 is ~$1,695 while the SP500 Intrinsic Value Index is ~$1,855. Most investors remain pessimistic even with new vehicle sales approaching all time highs, Retail Sales exceeding all time highs and housing market activity accelerating. Rising rates at this point in the economy gives banks the profit margin to expand their lending-spreads widen early in the cycle.

Markets remain attractive with this perspective which I believe to have more validity than most