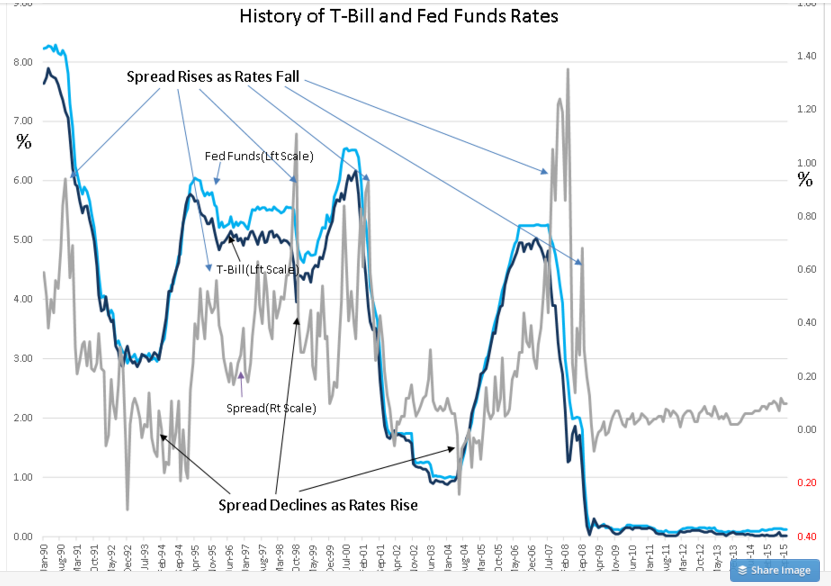

“Davidson” submits:

Historically it has not been the Fed who sets rates. Historically rates have been set by the market as investors adjusted their preferences for Fixed Income vs. Equities. The Fed historically adjusted the Fed Funds rates afterwards. The Fed is the ‘lender of last resort’ and therefore tries to keep its short term rates higher than the T-Bill rates by ~0.40%-0.60% to maintain market discipline. In the chart below, the Fed Funds Rate is shown as the LIGHT BLUE LINE, the T-Bill Rate is shown as the DARK BLUE LINE and the spread (Fed Funds minus T-Bill Rates) is shown as the GRAY LINE.

1) One can see this in the chart that when T-Bill rates rose coming out of past recessions, the spread between the Fed Funds rate and the T-Bill rate fell sharply. Often the spread has moved into negative territory as the Fed was slow to adjust its rates higher-see the arrows pointing out this detail. This was because the Fed would wait several months to make sure the rise was due to the natural demand for capital.

2) Typically the Fed is several months behind any change in rates only catching up once the T-Bill rate had begun to plateau.

3) When rates fall, the spread rises-see the arrows pointing out this detail- with the Fed again not responding to the fall in T-Bill rates till several months later.

It is the shift from T-Bills to Equities and business investments as investors gain confidence to seek higher returns which drives T-Bill rates higher. The Fed has never been able to force this shift. But this recession the Fed did something it has never done in prior recessions, this time the Fed performed a rate manipulation maneuver called Operation Twist. The goal was to lower mtg rates by lowering the 10yr Treasury rate on which the 30yr Conventional Mtg is priced. The Fed thought this represented easier credit. Historically the 30yr Conv. Mtg is priced at 1.6% higher than the rate of the 10yr Treasury. In my opinion, the Fed misunderstood the impact low mtg rates would have on lending institutions’ abilities to lend in a climate of increased regulation. The Mortgage Credit Availability Index indicates that mtg lending remains roughly at one-third the level which may be considered necessary for a full housing sector recovery. With increased regulation expense, low mtg rates represent tighter credit conditions. What is needed to expand lending are higher mtg rates so lenders can cover added costs.

Businesses and investors do not borrow at the Fed Funds rate. This is why raising the Fed Funds rate is not likely to have much impact on lending unless the 10yr Treasury rate also rises in response. Free Markets have always had greater power than government entities over the long term and I expect the same will hold in our current circumstances. Market psychology, however, is convinced at the moment that a Fed Funds rate rise is likely to slow economic activity and if the Fed raises its rate before T-Bills rise, then we could see some market volatility.

What we are likely to see once the dust settles is a higher 10yr Treasury rate which has already risen roughly 0.45% in anticipation of a 0.25% Fed Fund rate increase. Net/net is credit spreads between T-Bill and 10yr Treasury Rates have widened which improves lending conditions for financial institutions. Voila, 10yr Treasury rates rising faster than for T-Bills is good for an expansion in mtg lending and expansion of housing sector activity.