“Davidson” submits:

I repeat this investment theme because it tells us so much of what has been driving markets. It is mostly about what we think is occurring or about to occur than what is actually occurring economically. We have believed for decades that price trends reflect Supply/Demand and every change in trend has a simple economic explanation which has been reflected in prices. Our panic based on the belief that we had an ‘oil glut’ began as oil prices fell Jun 2014. However, I noted several times that excess inventories did not begin till Jan 2015, 6mo later, and as the US production pulled back from a July 2015 peak of 9.6mil BBL/Day to 9.1mil BBL/Day at the end of August 2015(corrected in 1mo), US inventories have stabilized in the 470mil BBL range (we have a seasonal swing of +/-20mil BBL due to winter/summer blend change-overs). Mostly investors mistake price trends for economic activity when price trends are due to market psychology. We see more often than not is a trend which is explained after the fact with reference to economics. Our markets the past several years provide a great example of our ‘Inflation Thinking’ and how it is this more than economics which has driven market prices.

Since 2009 when the Fed indicated its desire to inflate asset prices to stabilize prices, it initiated significant actions to expand monetary supply. These actions were based on Milton Friedman’s concept that:

“Inflation is always and everywhere a monetary phenomenon in the sense that it is and can be produced only by a more rapid increase in the quantity of money than in output.” The Counter-Revolution in Monetary Theory (1970).

The financial world has operated with this belief and an associated belief that the alternative cause of inflation is due to rises in oil prices since the 1970s. Yet, since 2009 we have had rapid expansion of our money supply and a sharp rise in oil prices ($40BBL early 2009 rose to $114BBL April 2011) and stable to falling inflation. Then, as if to underline the correlation between oil prices and our perception of inflation, oil prices declined from $108BBL June 2014 to $27BBL in Feb 2016 and inflation has risen from 1.5% to 1.9%. Little of what we have long believed regarding the sources of inflation or deflation have a correlation in our economic record since 2009. Recent economic data show our perceptions have been woefully incorrect. In earlier notes I have shown that inflation/disinflation come directly from changes in government deficit spending. Inflation is not correlated with the rises/falls in oil prices nor expansions of money supply. Our ‘Inflation Thinking’ needs to be adjusted. Contact me for a copy of earlier notes if you want to review.

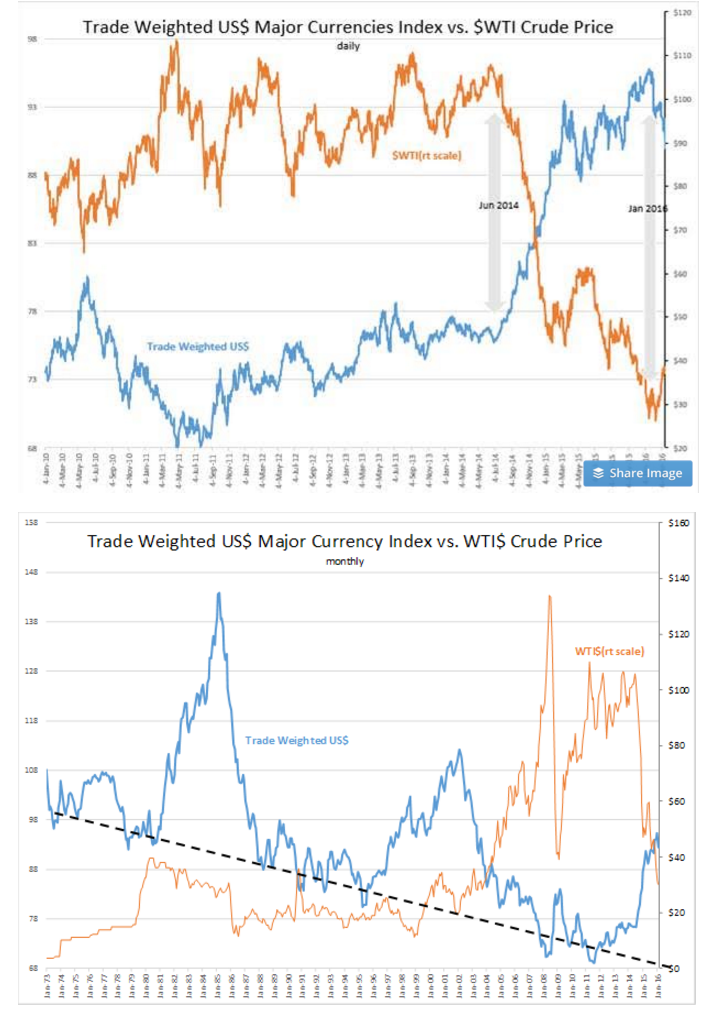

The recent collapse in oil prices coupled with US$ strength was due mostly to changes in investor market psychology ‘Inflation Thinking’ than due to collapsing economic activity which was so often highlighted in the media. It now appears that after more than 18mos of strengthening US$, this trend has reversed. The Trade Weighted US$ Major CurrenciesIndex now appears in decline towards its long term trend ~68. With the prominence of the US$ used in global trade, the correlation with WTI$ Crude Price and other commodities is to be expected. There is much discussion that commodity pricing including oil is connected to Supply/Demand but the last time this actually occurred is some point before oil became globalized, many decades ago. For many decades oil has traded like an alternative currency inversely to the US$. The daily chart Trade Weighted US$ Major Currencies vs. WTI$ Crude Price from Jan 2010 reveals a strong inverse correlation as does the chart from Jan 1973. But, we can observe that oil has increasingly traded with more volatility relative to US$ than in the past. Recent media reports indicate that oil-based derivatives are 17x larger than the crude oil available today. This is reported to be up from a 5x level in 2005. No wonder oil pricing vs. US$ Index is more volatile. The pattern we see is one in which the US$ shifts and WTI$ catches up.

The Trade Weighted US$ Major Currencies Index has a declining long term trend due to the US exporting our standards of living globally. As US trade grows, the importance of global currencies improves in value versus the US$. The sharp rises in the US$ in the past have always been correlated with the US GDP being stronger than World GDP. But, the most recent rise beginning in June 2014 occurred as investors fled to US$ as a safe haven when Russia invaded the Ukraine early 2014. Russia’s geopolitical activity triggered a much larger shift in market psychology which was heavily leaning towards expectations of inflationary pressures due to the Fed’s copious monetary easing. Considerable investment commitments favoring a weaker US$, higher WTI$ and higher prices for all commodities were in place. The Fed actively promoted such thinking with its purposeful pursuit of inflationary monetary policy. When Russia invaded Ukraine, investors, mostly Hedge Fund Momentum Investors, found themselves on the wrong side of a massive inflation bet. The inflation bet against the US$ suddenly had to be reversed. The US$ suddenly became much stronger and oil prices much lower.

The shifts in the chart are dramatically sharp!

Nothing in the investment markets occurs for a single reason. Markets if anything are messy. Usually we experience multiple themes which appear to be additive enough that they send investors in a single direction. The shift towards a strengthening US$ coincided with the belief that the US was over producing oil and that China was reducing its appetite for commodities. Momentum Investors shifted to avoid losses and took advantage of the new trend. US Treasuries also strengthened sharply and caused rates to fall back to historically low levels. The stories now emerging and the actual data do not support the ‘oil glut for years’, ‘most oil companies going bankrupt’ and ‘many banks will go under’ with which we were welcomed each day in the media. The 18mo trend of oil prices and US$ appear to have bottomed late Jan 2016-early Feb 2016. Neither severe inflation nor deflation has been experienced! Inflation averaged 1.66% for the period 2009-2016. Nor has there been a recession anywhere in the world!

The US$ shifting back to its long term trend. It is forced there by the activity of global trade which continues. Calls that global trade is slowing come from people who do not adjust for inflation. The Free Market continues at work. It is more powerful than market psychology, but it also takes longer to have its impact. Market psychology has shifted multiple times while economic activity has continued to grind its way higher. Market psychology works over months while Free Markets work over years. Seeing the differences in the impact of market psychology versus the economic trends is a good lesson for investors.

Investors can either try to catch the swings of market psychology and trade them or stick to economics and invest through the volatility. The problem with trying to catch Momentum is that it rarely makes sense economically. Momentum begins and ends without commonsense. Identifying turning points in psychology is truly impossible. Once you are sure of the trend enough to invest against commonsense, it turns against you. This is what most investors experience. As a Value Investor, I stress economic data. I stress hard economic data, the counts of things made, income adjusted for inflation and the counts of the number of individuals working. I ignore most sentiment surveys which includes those often given high regard in the media, i.e. the PMI, the Philly Fed Index, the NY State Mfg. Index and etc. There is little correlation between sentiment (market psychology) indicators and economic activity. Mostly what we see is that if the economy actually slows then people say they feel worse afterwards. Only well after the economy has recovered do people say they feel better. After the fact information is not very helpful to investors.

Today the US$ appears to be slipping fairly quickly towards its long term trend. This should benefit Natural Resources and Intl asset classes with more favorable pricing. Our economy has not missed a beat even with the many calls by market professionals for a new recession. When economic activity indicates that a recession is likely, history shows that the signals are present up to 2yrs before equity markets see a peak. No signs for a market peak are present today.

The best recommendation in my opinion is ignore the market psychology, follow the economic trends and remain positive.