“Davidson” submits:

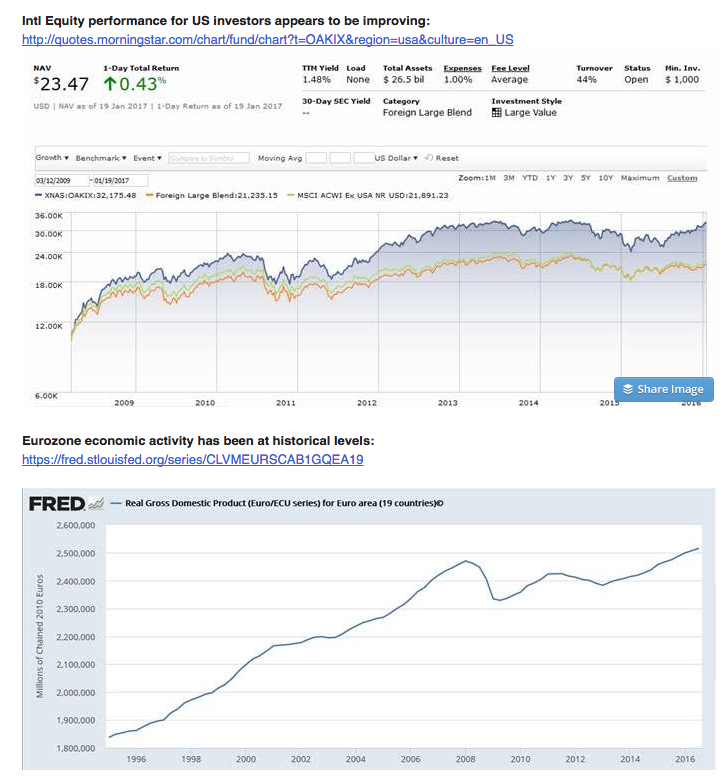

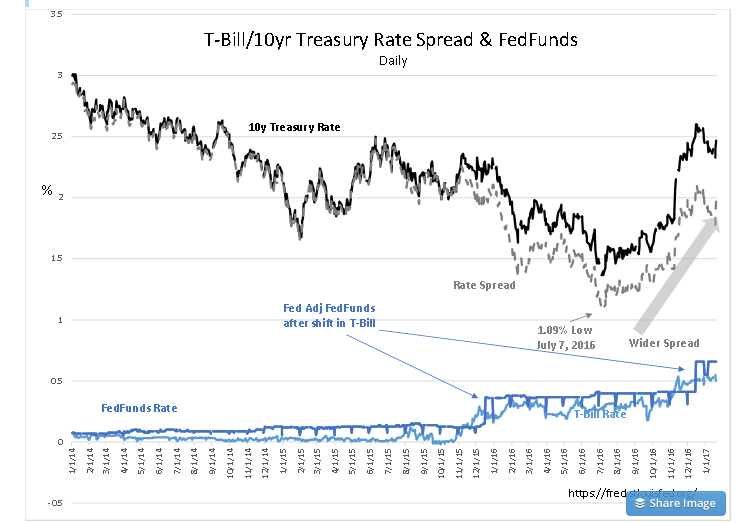

Market psychology does not always follow economics. This has been the case with Intl Equities. In the face of a rising US$, this category has underperformed the economic growth present in Intl Equities. That the Eurozone Real GDP has been growing at historical levels is shown in Real Gross Domestic Product (Euro/ECU series) for Euro area (19 countries). For US investors the impact of the strong US$ since 2014 has translated this growth into an under-performing asset class as represented by the price history of the Oakmark International Fund. Global capital flows impact currency relationships and are dependent on investor return expectations. Cause and effect for global capital flows are often connected to geopolitics and impossible to predict. Russia’s invasion of Ukraine in 2014, the rise of terrorism and autocratic governments in recent years has resulted in capital pooling in the US and other Western nations. The result has been excessive strength in the US$, rising real estate prices and historically low Sovereign debt rates. Ultra-low 10yr Treasury rates appear to be normalizing as capital begins its shift back to Intl Equities.

The recent performance of Oakmark International Fund and its Foreign Large Blend benchmark have improved in since July 2016. July 2016 was the low point of the 10yr Treasury Rate. I interpret this correlation as an indication that global market psychology has turned more positive since July 2016. Note that Intl Equities and 10yr Treasury rates peaked in early 2014 with Russia’s invasion of Ukraine. Today, it appears that capital which had previously pooled in the 10yr US Treasury has been shifting out of this position driving 10yr Treasury rates higher resulting in higher prices for Intl Equities for US based investors.

Predicting swings in market psychology is an impossible task. The best I think we can do is to anticipate economics using current indicators relative to historical data and then verify that we are in roughly the right place with portfolios by selecting the better portfolio managers and CEOs as investments. Even then, over the short-term, market psychology can ignore economics till it has run its own course, the extent of which is unpredictable. History reflects that economic activity and relationships of market prices to business returns eventually normalize. I interpret the recent rise in the 10yr Treasury rates with the rise in Intl Equities as the early stage of normalization.

Oakmark International Fund is being used as an example for this discussion. There are at least a half-dozen qualified alternatives and I recommend that investors diversify across as many qualified managers and CEOs as portfolio capital will permit. I have recommended investors have exposure to Intl LgCap Equities since 2009. I have recommended adding to these positions multiple times the last 2yrs as they appeared go be good values. I continue to recommend portfolios consider 30%+ exposure. When markets fully normalize, I expect portfolios to benefit.