“Davidson” submits:

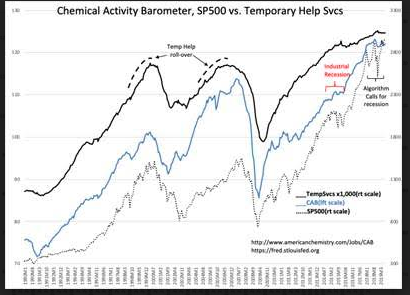

Job Openings and Temp Help indices are good indicators of the demand for labor. There are multiple drivers behind employment trends with shifts in industry demand across every economic cycle which do not repeat cycle-to-cycle. Each cycle has its own themes which requires that investors to educate themselves as economic activity evolves. One can never assume the past will repeat. Current trends follow this rule.

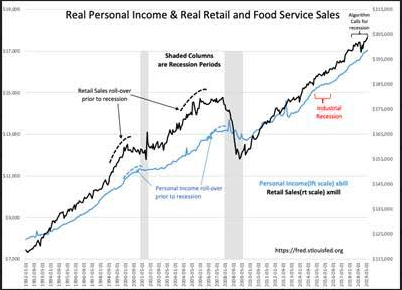

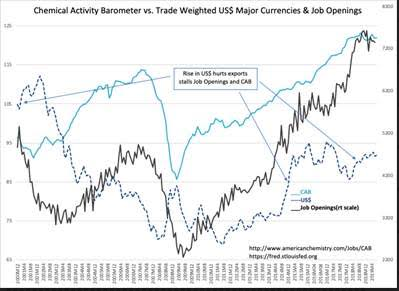

Job Openings and Temp Help have stalled this cycle for the 2nd time. The charts relate correlations between these indicators, the Chemical Activity Barometer(CAB), the Trade Weighted US$, Retail Sales, Personal Income and the SP500. The key point of reviewing multiple trends together is to identify the stalls in Job Openings and Temp Help are connected to the strength in the US$ and not general economic activity. US$ strength makes export goods less competitive and thereby reduces US manufacturing demand for labor. The CAB index also stalls with strong US$ periods as it reflects slowing chemical/plastics manufacturing for export. The observation that the US economy remains in expansion comes from Retail Sales and Personal Income trends remaining intact.

A decent portion of employment growth has come from the recovery of US manufacturing sector which is export price sensitive. What has been impressive has been the resumption of manufacturing employment growth after adjusting for the 1stperiod of US$ strength in 2014 which culminated in US oil prices plunging from $100+/BBL Jun 2014 to less than $30/BBL in early 2016. The US posted a record Household Employment Survey for July 2019 which is the basis for Personal Income and Retail Sales. Current expectations are that we should work through the current period of increased US$ strength and resume labor demand for US manufacturing