“Davidson” submits:

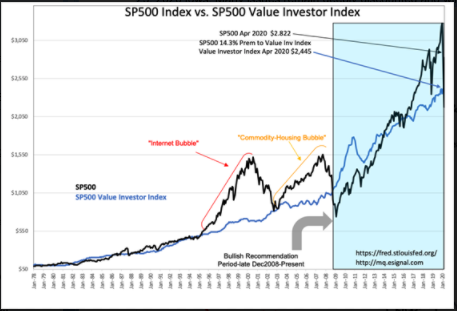

The Dallas Fed reported the 12mo Trimmed Mean PCE(Inflation) of 1.96%. This represents a 0.08% lower value than reported the previous month. The COVID-19 panic brought the SP500 to ~11% discount on April 23, 2020 but has since rebounded mostly due to Momentum Issues to ~14% premium. The top 5 mega-cap momentum driven issues comprising ~20.5% of the SP500 are responsible for the sharp rebound. The other 495 issues reflect varying levels of rebound with most not rebounding at all at this point. Markets are unequal performing composites. The Momentum Issues always drive markets higher during prolonged cycles leaving investors wondering where is their performance. When asked if they want to own the high-fliers they respond “Too risky!” but then continue to question performance.

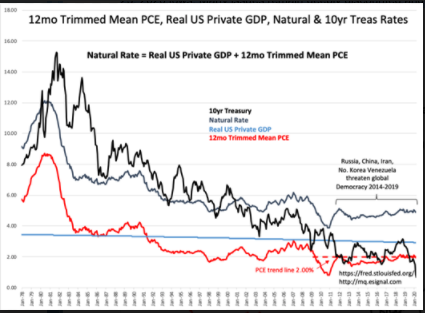

The Natural Rate is 4.9%. The 10yr Treasury rate tracked the Natural Rate benchmark with a premium since 1978. Then in the late 1990s foreign capital began a long-term shift to US$ assets and drove 10yr rates below the benchmark. With today’s panic, 10yr rates are 0.06% or 5,000yr lows reflecting the panic of COVID-19’s economic impact. Foreign capital has pooled heavily in US$ denominated assets, mostly Treasuries. It is a sign of extreme fear which makes equity prices today very cheaply valued once this pessimism eases.

The pace of countries and individual US states to restart economic activity is picking up. The news on COVID-19 treatments is positive and can act as a stopgap till vaccines are available. The pace of vaccine development has never been as rapid as today. Some expect to be available in a few months as opposed to years. Market confidence should follow the pace of economic reopening and news that we have COVID-19 controlled. The SP500 has already rebounded ~30% from April 23, 2020 lows. Many issues remain deeply discounted and will look much better in the light of increased economic activity.

Buy equities!