“Davidson” submits:

Every forecast leans defensive when expanding rate spread indicates a more aggressive investment stance. The question is more where one should invest, not if. The ‘where’ is in industrial companies supplying the infrastructure underlying economic expansion. My analysis leans far away from those companies previously COVID-favored as still very over-priced i.e., AAPL, NVDA, FB, AMZN, TDOC, ARKK, DUCU and etc. Violent corrections in these companies the past 5mos have panicked many that recession is imminent. But, these companies were ridiculously over-priced and represented a very narrow focus of the market as if they represented the entire market. Their revenue ‘growth’ was accepted as true economic growth when everyday they are revealed as having been simple ‘flashes in the pan’ as in Peloton. Revenue growth w/o Net Profits and growth in shareholder equity being called “Growth” is magical thinking.

The undervalued remain companies to benefit from higher energy cost or able to adjust to the same. E&P companies and related industries with decent insider buying deserve a good look. But, there remain companies which have been battered by, in my opinion, algorithmic shorting which are likely to benefit as certain parts of the country have yet to reopen i.e., auto-parts suppliers, fossil fuel infrastructure cos, construction and some retail.

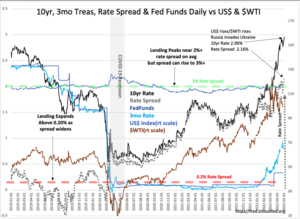

One wants to buy growth directed by skilled management teams priced at a steep discount with recent insider buying or optioned-share accumulation. The rate spread expansion to 2.16% is very positive and indicates businesses sifting capital into productive and income producing assets. The auto, Class 8 truck and aircraft mfg industries have high demand vs low relative production which will require a couple of years of catch-up.