Given people’s outlook, a GOP wave in the midterms could lead to a big market rally

“Davidson” submits:

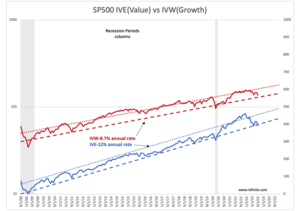

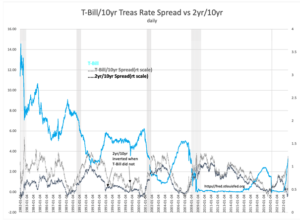

There is a very old phrase which applies to market prices which are at all times a reflection of consensus perception. Its origins are so part of our thinking that its roots in various forms likely pre-date the earliest known philosophers. The phrase or variations thereof, “Shutting the barn door after the horse has bolted is useless” is apt for this market. Two data series, SP500 IVE… and T-Bill/10r Treas… are good illustrations for understanding the current market.

The first chart from 2006, SP500 IVE…, should make it clear that both Value and Growth issues as represented by representative SP500 indices are at or near historic lows of prior recessions. If one compares advisor guidance then with now, the identical level of fear of further declines is apparent. The Bank of America Fund Manager Survey recently released indicates a new record level of pessimism since the inception of report in 2002. There are other reports indicating 90% of managers are pessimistic. Couple this with the second chart from 1982, T-Bill/10r Treas…, indicating that the traditional pattern of investors piling into T-Bills forcing their rates lower has not occurred. What has occurred is that T-Bill rates have soared. A highly unusual response to high levels of pessimism.

90% pessimism is the very one-sided market position. It is so one-sided that the level of portfolio hedging exceeds all previous levels. This has occurred to such a degree that it appears reserve capital normally stored in T-Bills instead now resides in bets of further market declines. I term this as ‘speculative hedging’. Not only does the first chart indicate pricing already reflects prior periods of extreme pessimism, but numerous businesses involved in core economic growth report high demand for products and services. This is an unusual condition of consensus price-trend-following being well out of sync of economic fundamentals. For thoughtful investors this forms an unusual investment opportunity.

The consensus is making the same gross error today that has been made for millennia. The current declines are and were never warranted. Investors are best advised to add equities and to avoid fixed income. My approach is to select companies at discounted Pr/Sales levels relative to their financial histories. The likely price multiple expansion once market participants recognize fear is grossly overdone can prove significant.