“Davidson” submits:

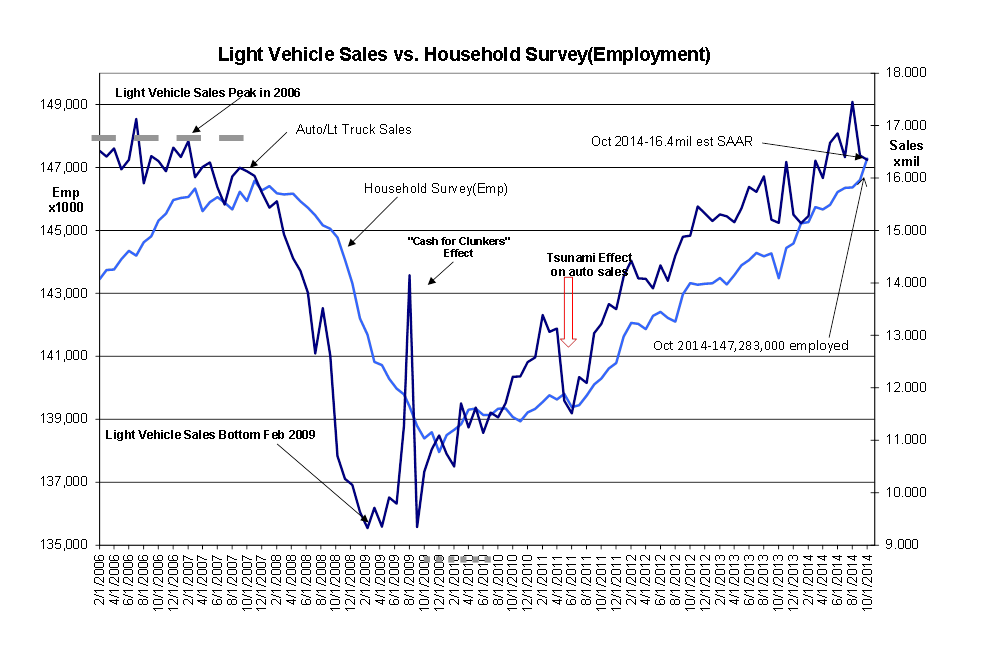

This week 2 key economic trends saw trend extensions. Light Vehicle Sales came in at 16.349 SAAR(Seasonally Adjusted Annual Rate) and the Household Survey (Employment) came in 683,000 higher. What the media tends to focus on are the ADP and Establishment Employment reports which do not cover the entire population. ADP does not cover Government Employment which is included in the Establishment report, but neither make estimates on those who are self-employed which is included in the Household Survey which seeks to measure total employment. Previous figures for the Establishment report saw revisions higher by 31,000. The Household Survey is not revised monthly. Regardless of which one uses, it is only the trend which is useful and not the month-to-month change. The Household survey one should always be aware carries a statistical error of +/- 436,000. While this appears to be ridiculously large, it is really the error on the count of 147,283,000 employed or 0.3%. Only when our focus is on the month-to-month change does it appear large and it is why seeming to make predictions and trade on month-to-month reports is a useless endeavor in my opinion. The odds of making the ‘right trade’ any month is quite low and the odds of making a series of ‘right trades’ is extremely low. The odds however of investing successfully with the trend over the long term are quite high in my opinion.

As the chart of Light Vehicle Sales and Household Survey data shows below, trends continue higher.

Historically, the correlation between economic expansion and higher equity prices/lower fixed income prices is quite strong if one looks across the cycle. Most investors fail to see this relationship precisely because they are looking too closely at monthly detail and fail to see the broader relationship. Why they do this is in my opinion related directly to the demand by the majority for greater and yet greater parsing of data into trading strategies which reduce ‘Risk’. When the term ‘Risk’, that is risk with a capital ‘R’, they mean volatility which was placed into its current definition by Harry Markowitz, a mathematician and Noble Prize winner for this interpretation, in 1955 with what was later named Modern Portfolio Theory. Unfortunately, investing was forever changed as mathematics dominated thinking ever since.

The reason mathematics has failed to reveal the secrets of investment markets(or any market for that matter) is that markets are human systems and lack precise relationships and the relationships which exist also have changed over time. Market prices are set by participants based on pure psychology. Prices are set by what the average investor and often pure speculator on where they think market prices are headed minutes and hours ahead. My work shows only two types of investors, Value Investors and Momentum Investors. Value Investor psychology is based on long term comparisons between GDP growth and the higher long term growth which is available to them in earnings and Shareholder Equity of corporations. Momentum Investors employ short term price trends lasting from minutes to months. While they may speak of ‘Value’, Momentum Investors are price trend investors. The markets reflect both approaches. Further, markets operate by collections of rules designed to inspire ‘fairness’ between buyers and sellers. But, these rules have been adjusted as markets evolved. Using mathematics to analyze market prices has been, is currently and will forever prove a fruitless enterprise. Mathematics alone cannot and never will be able to predict human psychology.

What historical study does reveal is that market psychology over the long term rises and falls with the economic trend. In fact as long as one is not trying to trade markets short term, but instead seeks to identify the major turns in economic activity across what more recently has been 10yrs+ economic cycles, then one, in my opinion, can make prudent decisions and achieve respectable gains in one’s portfolio.

Bottom line: Trends continue to support a strong bias to equities ($SPY) and against fixed income. I remain very positive.