“Davidson” submits:

One means of understanding the details of our own economy is to dig into the details and see what emerges. Previous notes have focused on various economic trends which indicate economic expansion in the broad economy even with housing and construction only just lifting off. Yet, many continue to bemoan the economic weakness especially in US employment and our GDP. Only looking at the top line fails to reveal the dynamic economic changes which represent the healing of economic excesses during the sub-prime period.

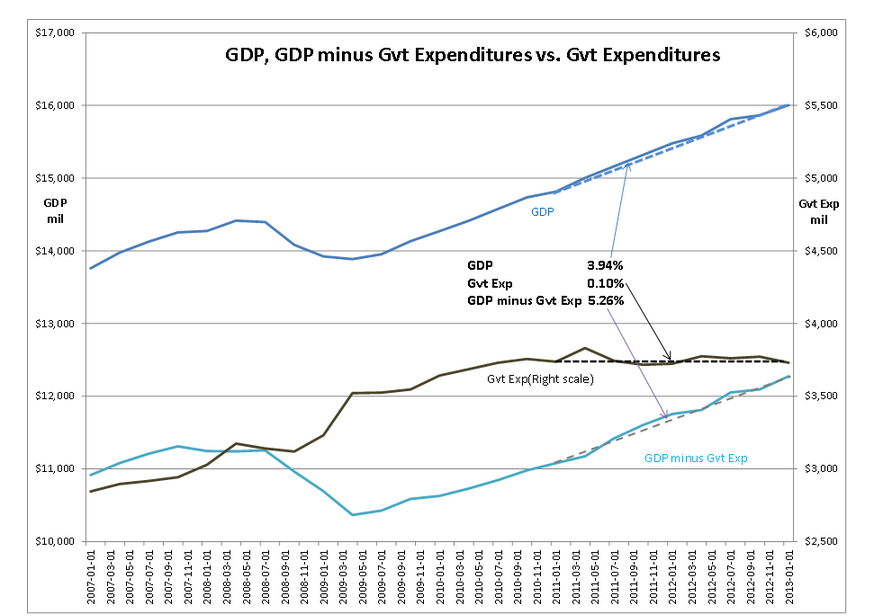

Two charts below represent the dramatic differences in the private and government sectors of our economy. The first chart looks at US GDP and GDP adjusted for Government Expenditures while the second chart looks at the trends in private employment vs. government employment. Together, these charts reveal that a vibrant economy is actually bubbling along while excess government is being corrected.

In the chart, GDP, GDP minus Gvt Expenditures vs. Gvt Expenditures, I subtract the consumption due to government from our GDP so that I can calculate the growth rates of the two segments of our economy(commonly accepted practice). Recent history shows that government spending had been in the 18%-19% of US GDP range and that the rise to ~25% during the “Great Recession” was very troubling. Many have blamed slow GDP growth on the burdens of government.

We measure economic growth using GDP and Real GDP(adjusted for inflation). Inflation today using the Dallas Fed 12mo Trimmed Mean PCE is 1.3%. The current US GDP pace since 1Q11 has been 3.94% as can be seen in the chart which becomes a Real GDP of 2.64% when inflation is subtracted. US historical Real GDP since 1985 has been 3% with recessions falling to ~2% growth and peaks rising to ~4% growth. We typically view GDP and Real GDP as including the whole country, i.e. private sector and government sector combined. But, when one looks at our present situation by subtracting the government portion of GDP to reveal the non-government private sector portion of GDP, surprise, surprise, we find that the private sector since 1Q11 is chugging along at 5.25% GDP or a Real GDP growth of 3.95%. What is being missed by many is that government spending has been nearly flat since 1Q11(0.10% annual growth) while the private sector has shown a sizable recovery. So where are jobs?

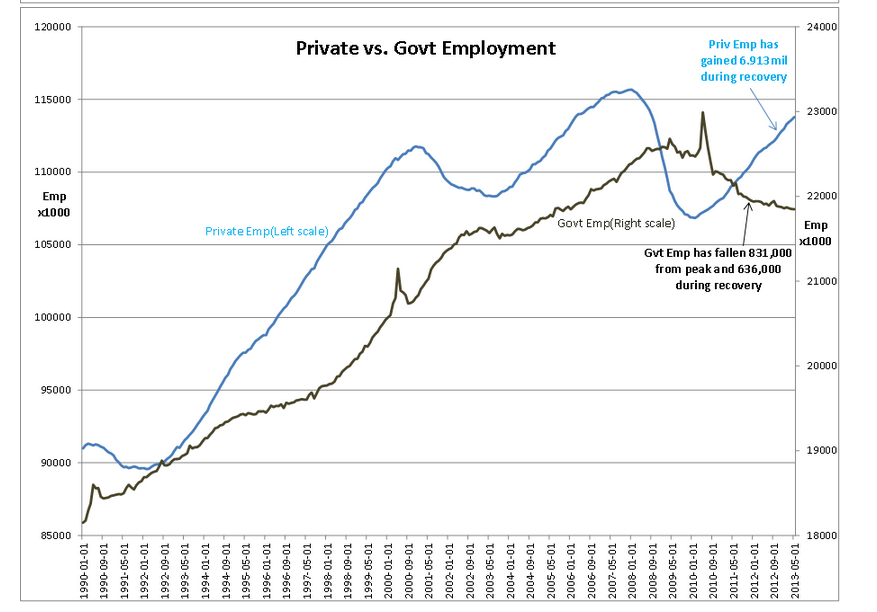

Turning to the second chart, Private vs. Government Employment, one can see that government employment has shrunk 831,000 from its April 2009 peak (the spike in 2010 is due to temp. hiring for the Census) and lost 636,000 while the private sector gained 6,913,000. This data comes from the Establishment Survey and does not count the self-employed. If one uses the Household Survey(my preferred employment measure) one can see a healthy trend of ~280,000 newly employed per month pace since July 2011(see last weeks note).

While we remain behind expected historical GDP growth and employment trends, the reasons for this lie within the correction of an overly large government sector. The private sector is indeed carrying all the burden of our recovery and its strength is partially hidden by the contraction in government.

The reasons for being optimistic at this time of additional media doom and gloom come from the obvious recovery in housing and construction which have 5yrs of pend-up demand to work off with additional economic expansion and the knowledge that government contraction will stop at some point. Combine these historical trends and we can expect a sudden surge in GDP and Real GDP in the coming years which will surprise many. Precise estimates of GDP, Real GDP and in which quarters to expect them are impossible to predict as are all economic data points. The best we can do is to observe the trends, but this does not stop us from investing with confidence.

Optimism is warranted in my opinion with the focus being towards equities and away from fixed income(except for selected asset classes) LgCap Domestic and International equities continue to appear to offer the better future returns ($SPY).

One reply on “The Private Economy is Doing Just Fine”

[…] The private economy is doing just fine. (Todd Sullivan) […]