I promised more on this so here it is:

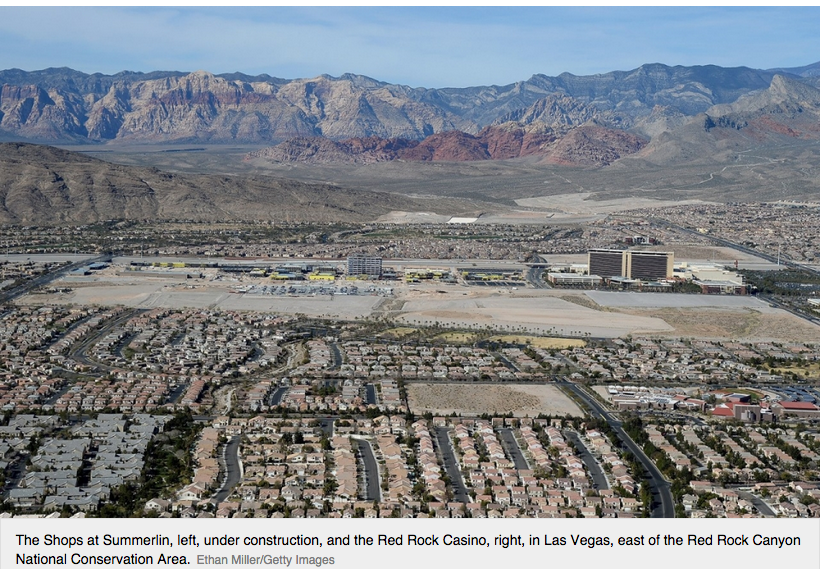

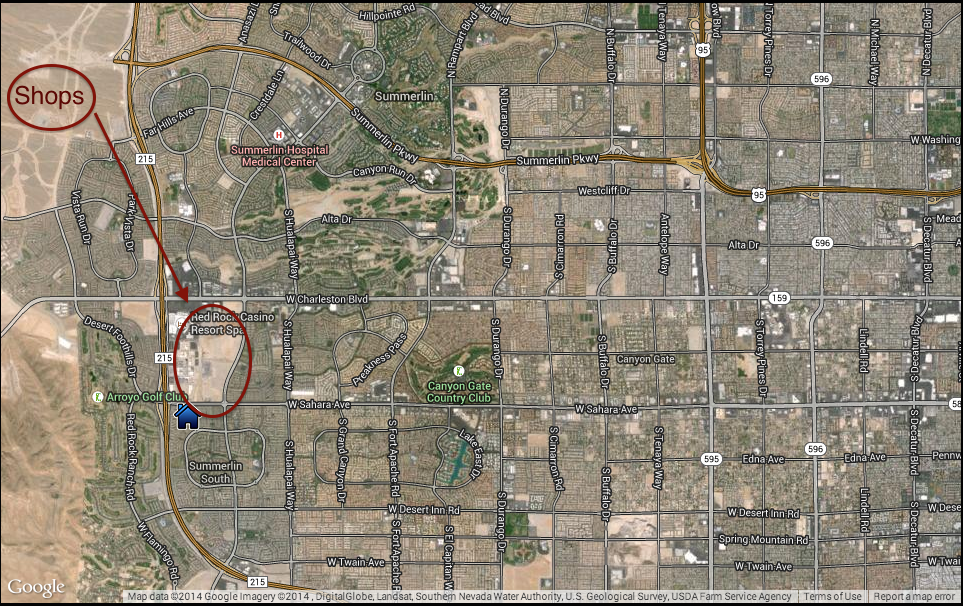

Let’s start with the basics: Downtown Summerlin will be approximately 1.6 million square feet and will consist of a 1.1 million square foot Fashion Center which is designed to have three anchor tenants, small-shop retail and restaurants. Additionally, the project will include an approximate 200,000 square foot office building and approximately 280,000 square feet of big box and junior anchor retail space adjacent to the Fashion Center Here is the location visually (before construction finished):

Remember, currently only 1/4 of the site is being used for the above project (1.6M sqft) and the aerial view below shows the mass of residential development around it (the area to the left is residential still to be developed by HHC who has entitlements for ~42,000 more homes). Here is a drone view of the project, towards the end of the video you can see the land just waiting to be built on.

The first thing one notices when you talk to people from $HHC about Downtown Summerlin is the satisfaction they have in what they built. It would have been easy to slap up yet another non-descript rectangular mall that would have garnered excitement for a bit. What they instead built was a destination. They built a place people will want to go to for high end shopping, dining and entertainment for years, not a place people grudgingly go to because they need something at the store. The best part is $HHC owns all the land surrounding the project so competition will be scarce. Further as the project is expanded and further built out, its draw will increase. It is the same thought process going into the S. Street Seaport in NYC

Now, currently Summerlin has 41,000 homes and ~100k residents and that is served by 2.1M sqft of retail. The retail that is currently there is nothing like Downtown Summerlin but rather the usual smaller strip malls/restaurants that dot most US communities. It is estimated ~$2B in annual retail sales leak from Summerlin to other parts of Nevada. An ancillary effect of Downtown Summerlin is that the retail and office space make the remaining residential lots to be developed more valuable. The company put 1.6M sqft of retail/office space on 1/4 of the available acreage. It doesn’t take a math genius to figure out they could add another 4.8M sqft to what is left. This of course assumes they avoid doing one VERY obvious thing….go vertical.

The current floorplan is two stories high retail and a seven story office building (a 124 unit luxury condo building is coming). Think higher (and deeper for parking) going forward as the shops all open and the current office tower is filled. More office towers that feed the retail will then need a hotel (they are currently building and will operate at 302 room Westin in The Woodlands). Another luxury condo tower would fit nicely to compliment the retail, office and $1M plus homes in the area. Let’s not assume even for a second that what sits there now for retail satiates the demand. Having seen the site it is perfectly set up for much much more retail development even to just enlarge to current project. The $40M NOI for ’15 will be a distant memory in short order.

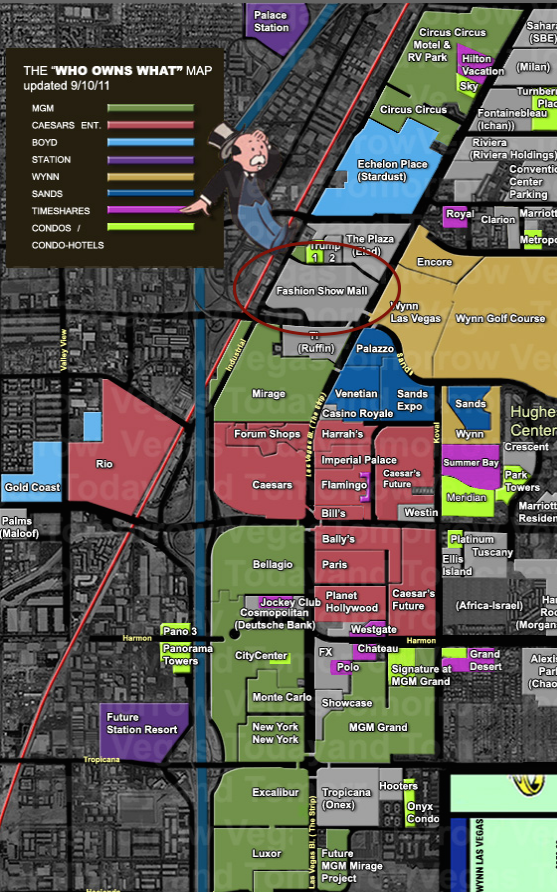

The bottom line is the eventual sqft of the operating assets on the 400 acre site in my opinion will be will be much more than most folks now assume. Now, if we are going to take a billion dollars or so of retail sales off the strip, what is the Fashion Show Mall on the Vegas Strip going to do? Given its convenient location to the highways on the strip and stores in it, currently it is drawing the same shoppers from Summerlin that will now stay in Summerlin to shop rather than fight strip traffic. This is where things get interesting. Check out the following map (fashion show in red next to Monopoly character):

Now that City Center is done (Aria, Mandarin and Cosmopolitan), the ONLY place left on the strip to go UP, is the Fashion Show Mall (red circle). There is room to go other places, but they are either off the strip or at the extreme ends of it. The Fashion Show is right across from the Bellagio/Pallazzo and the Wynn and next to Treasure Island/Mirage. So, it makes perfect sense to redevelop the fashion show and add a hotel/casino right on top of it. If you’ve been there you know it is a simple 3 story facade shopping structure fronting a mall behind it.

If you want to go up, you just need to know who owns the air rights. Who owns the air rights above the Fashion Show? Howard Hughes ($HHC) owns 80% of them. So, if we follow the playbook they have been using, how would this go? Typically what Hughes has been doing (see below) in these projects (except for Downtown Summerlin, S. Street Seaport and a few other larger projects) is they contribute the land they own to a JV with the developer at a certain valuation and then take 50% of the project (office buildings etc). If we then used this here, in theory they would contribute, air, at a valuation of “x” for their contribution to the JV (and prob a bit of cash in this case due to the size of the project).

Now, skeptics will scoff at this and question just how much air is really worth but when one considers that air will then be filled with a Vegas hotel/casino, I’d say in this case “air” has quite a bit of value.

So the next time someone says to you “money just doesn’t appear out of thin air you know….” ,well, tell them for shareholders of Howard Hughes, it really sorta does.

Back to Downtown:

From the Las Vegas Review Journal

The opening of Downtown Summerlin will dramatically change the commercial real estate market in Southern Nevada, five senior industry executives agree. But they differ on just how those changes will be felt in the valley’s submarkets. The five — Michael Newman, managing director of CBRE; Frank Gatski, president and CEO of Gatski Commercial; Paul Chaffee, partner, NAI Vegas; Jeff Mitchell of Virtus Commercial; and Scot Marker, senior vice president of Colliers International — each fielded questions in the Business Press’ “virtual round table” format. Their responses have been edited for space and clarity. Here’s what they had to say:

Q:How does Downtown Summerlin change the commercial real estate market? Newman: The opening of Downtown Summerlin sends a big signal both nationally and locally that the Las Vegas economy is recovering. It is the single largest development in the valley since Town Square opened in 2007, and it is one of the country’s three largest projects under active development. Downtown Summerlin will offer a new and unique destination for shoppers, diners and entertainment seekers around the valley and attract some brands that aren’t currently operating here. It’s an exciting new venue for the entire valley given its accessibility via the 215 Beltway. Mitchell: Downtown Summerlin is a dynamic factor for change in the Las Vegas commercial real estate market. It serves as a beacon market indicator to the national real estate industry that Las Vegas is viable and is creating new growth opportunities for retail, based on demand from retailers for a high-caliber, large-scale, non-resort-corridor retail project. This signal is positive broadly as it also carries into the office, investment and industrial sectors. Secondly, Downtown Summerlin and the closely proximate Sahara Center (at Sahara Avenue and Hualapai Way) add a substantial quantity of retail space to the West Valley submarket. This places additional pressure on more established retail centers such as Boca Park — the most productive sales/square foot retail project off-Strip — Village Square, Tivoli Village (still experiencing some growing pains) and even Fashion Show mall to stay competitive and continue to create unique opportunities for customers and retailer success. Thirdly, Downtown Summerlin shifts the focus away from strip retail for brand growth combining large department store anchors and compelling lifestyle components. This is something that Forest City’s Galleria at Sunset mall has failed to fully realize in Henderson. The Downtown Summerlin project will be a paradigm shift for the commercial real estate market. The retail needs for the Summerlin populous should be met by this project, redirecting shoppers from the Strip to a more localized shopping experience. The Downtown Summerlin project will also drive office and tertiary users into the Summerlin area, as the project will direct a high volume of customers. Gatski: Downtown Summerlin will shift the retail and entertainment focus for local residents particularly on the west side of town from the strip to a more localized friendly venue. It creates a benchmark for future development not seen for decades. Downtown Summerlin is a positive sign of both investor confidence and consumer confidence for the entire Southern Nevada commercial real estate market.

Q: At what point are we in danger of becoming “overretailed”?

Marker: I have been asked this question for years but I’m not sure if this will ever happen. I believe the strong retailers will always evolve to address the changes in consumers’ needs and buying habits. Will we ever grow tired of the latest model of anything? Whether it is a car or a mobile phone, there will always be a desire to obtain the “new and improved” version of a product. A better question may be, how do we retenant vacant spaces in transitioning trade areas? As our neighborhoods get older, the residents change and so do their shopping needs. Shopping center owners need to be aware of their neighborhood and the needs of those who live there.

Mitchell: Staying with the theme of Downtown Summerlin, the old adage is that “retail follows rooftops” and new rooftops are rapidly underway in Summerlin. The growth is not speculative. And, from a demographic standpoint, this growth is population-based and our economy continues to grow beyond the recession rebound. Retailers understand this dynamic and seek to capture the disposable income. Downtown Summerlin is perfectly situated to capture demand in a synergistic anchored retail environment. The market will also determine if we are overretailed — survival of the fittest. Marketwide, unanchored retail is always the most at risk. As with most new large retail projects, there will certainly be fallout of retail tenants in the first couple of years. Downtown Summerlin will experience a stabilization period. National retailers will likely weather this phase; mom and pops will have a harder time — it’s a function of capital. Food and beverage is also acutely at risk. This area is highly competitive and margins are tight, especially with continued labor cost increases, I anticipate several second-generation food spaces at Downtown Summerlin in the next 24 months.

Gatski: If the Southern Nevada economy continues to grow at a sustainable pace and investors and developers look at the supply versus demand, I believe we will be able to continue developing retail at a pace that keeps up with demand with minimal concern of becoming “overretailed.” Hopefully we’ve learned from the mistakes made prior to 2008.

Newman: I don’t think we are in danger of becoming “overretailed” in the foreseeable future. National retailers are generally well prepared in their evaluation of markets and individual location criteria. It’s the local retailer that sometimes doesn’t have the financial and analytical resources that the big national or regional folks have. As a result, we see more turnover with this class. When times are lean, the local retailer may not have the financial ability to weather the storm to better times. That said, I think the tough times are gradually passing and I expect retail will continue to gain strength. Overall, the market has seen about 1.5 million square feet of positive absorption (a demand indicator) over the past three years and the vacancy rate has decreased by about 360 basis points from a high of about 14 percent in 2011 to about 10.4 percent in the second quarter. We will probably see an increase in vacancy, as a result of a few Target store closures. Downtown Summerlin is not going to cause “overretail” in the market but will enhance the product mix that is in demand for the Summerlin area and, to some extent, the entire valley.

Q: What is the outlook for retail space that’s vacant today?

The Las Vegas retail market continues to improve, albeit at a moderate pace. First quarter 2014 showed vacancy rates holding steady from the previous quarter with modest declines for the 11th consecutive quarter to reach the lowest vacancy rate in approximately five years. Net absorption was positive once again as it has been for nearly two years, a trend that has occurred quarter after quarter within the same time frame. Sales volume rose in fourth quarter 2013 with averages at $88 per square foot over third quarter 2013 with averages at $129 per square foot. First quarter 2014 produced sales averages of $114 per square foot. Construction activity continues across the valley, the effect of which will be interesting to see as we continue to monitor demand. With positive indicators within the Las Vegas economy showing signs of stabilization and an improving job market with retail and hospitality leading the way, it appears that there is a strong probability that the demand will be able to keep up with the forward supply of product expected to hit the market in 2014.

Newman: That’s a tough one.

A lot of the vacant space today is in areas or neighborhoods that have made a demographic shift in the last 10 years, causing many tenants to relocate or cease their business. This has left a number of empty grocery store shells and few alternative uses. Retailers rely on grocery anchors to drive traffic so, when the grocer (or other anchor) leaves, the remaining tenants struggle. We have seen some grocers with an ethnic emphasis go in behind and fill the vacancy, but there is only limited opportunity for this. I think well-located and well-designed centers will continue to prosper but many centers that are located in the center of our community may take a long time to infill. In some cases, that infill may come in the way of a redevelopment of an alternate use. We have seen several big-box retailers, namely Target and Albertson’s, close underperforming stores, however landlords and sublessors have been flexible to find possible alternative uses (call centers for example) or demise the space for retailers requiring smaller footprint. The market has been bifurcated with strong leasing in the Summerlin, Henderson, to some extent the northwest, but the central core area is still suffering from high vacancy and is ripe for redevelopment or repurposed for other uses. Another interesting trend has been the influx of medical users leasing space in retail centers. This is a result of medical users taking more of a retail approach to location analytics opting for accessibility, and visibility than being located in traditional office locations.

Gatski: We have seen vacant space being absorbed at a rate close to that of 2006 and 2007 again. With the strengthening of our local economy, coupled with that of disciplined development, the retail vacancy rates will continue to drop over in the near future.

Marker: The owners of vacant space in our market need to evaluate their product to determine a viable tenant or tenants. In some cases, this is not always going to be a retail user. This will become a bigger challenge as Las Vegas grows and matures. Another factor that will impact shopping center vacancy is the use of the Internet by major retailers to sell their products.

Q.: What area is going to be hot for retail in 2015?

Mitchell: Summerlin, Southwest and Downtown. Long range, Henderson Galleria area will see further growth with Union Village being a major catalyst. Marker: In regards to shopping environments, open air centers will be hot. Open-air shopping experiences have been the trend for a number of years and they will continue to evolve. As a common trend, many consumers are drawn to the feeling of being in a downtown setting that is buzzing with activity, like many urban environments such as the Gaslamp District of San Diego or Union Square in San Francisco. We have already seen a few versions of this concept locally. Initially, we had The District in Green Valley, which was actually an evolution of the Green Valley Town Center back in the mid-1990s. Both centers were developed by America Nevada Co. Then came Town Square, developed by Turnberry, which raised the bar substantially and now we are lauding the opening of Downtown Summerlin. Change is seemingly constant. I believe that the surround area of the Downtown Summerlin project will be hot as well as the Chinatown/Asian market corridor along Spring Mountain (Road). The Strip is always hot and will continue to be so. The strip centers within the new home developments in Inspirada and Mountain’s Edge will continue to grow as the market recovery continues. Also, with the limited amount of available distressed retail properties, I believe we are going to see higher trade values for distressed properties in traditional sales and auctions.

Newman: Path of growth areas like Summerlin, ease of access locations along the north and south beltways and locations within the resort corridor should continue to thrive as new home development continues to grow … but keep in mind that we’re not expecting “explosive” retail growth. We will continue to add and improve but at a slower pace. The Southwest will see some growth as result of the Ikea store, and ancillary retail projects built around that area to take advantage of the additional traffic. Retail follows rooftops and we will likely not see significant retail development until 2016 and beyond when new home communities start to build and sell.

Q: Dust off your crystal ball and give us a prediction for the retail vacancy rate and average price per square foot — across the whole metro area — at the end of 2015?

Gatski: Looking into the proverbial crystal ball with an optimistic eye, it wouldn’t be surprising to see retail vacancy rates fall below 12 percent overall and drop into the single digit (percentages) in some submarkets. This will take into account new construction that will keep the number somewhat artificially inflated. The average price per square foot has steadily been moving away from the unrealistic benchmark of $1 per square foot that’s permeated the market during the recession for many neighborhood shopping centers; we should see this rate climb closer to an average of $1.25 to $1.50 (net-net-net) overall and over $3 per square foot for certain retail locations by the end of 2015.

Mitchell: 7.3 percent; $1.40 per square foot per month

Marker: Rates and vacancy in most areas of Las Vegas will remain the same. The economy will continue its path of slowly getting healthier. We will still see centers in the older neighborhoods struggle to lease their vacant spaces. Some large vacant boxes will remain empty (because of) lack of demand. In the Las Vegas retail market, there are a few centers that could truly benefit from creative owners with capital to rebrand or repurpose their center’s image and increase lease rates and lower vacancy. It just takes time and a team that is focused on the same goal. Although with have a dynamic and fluid market, I believe that the retail rental rates will rise by 5 cents to 15 cents per square foot (net-net-net) into the end of 2015 while vacancy rates will continue to decline as consumer confidence rises.

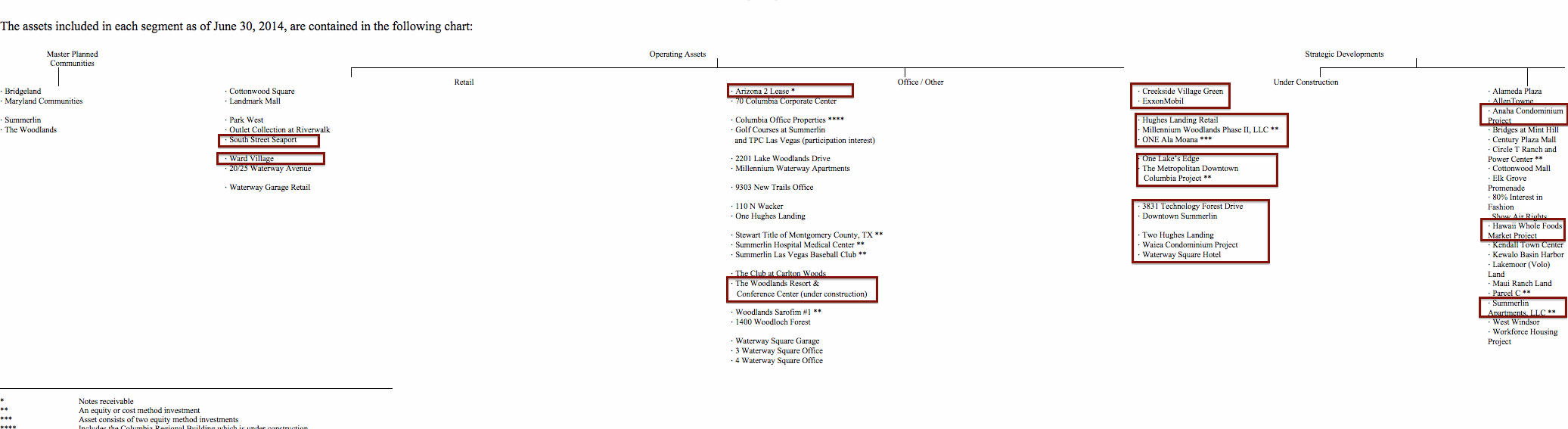

Now lets take a look at the rest of the operating properties….(Note: the following discussion excludes residential land sales for Hawaii, Summerlin, Woodlands, Bridgeland, Columbia and West Windsor)

Those is red are currently under construction/redevelopment and are scheduled to be either entirely or majority opened in 2015 and 2016. Right now the company sees ~$18M per quarter in NOI from what they have (Downtown Summerlin ought to add $40M NOI in ’15). It is really important to note this current $18M ($70M-$80M annual) excludes a finished S. Street Seaport which at NYC rents could easily see $400sqft (low balling) on its 385k sqft of retail space adding another $154M in annual rents and another $60M-$70m in operating income to the party.

If you look closer at the list you’ll see the Exxon projects, Ward Centers in Hawaii and the closing of the first two luxury towers there. It also excludes any other projects announced between now and the end of 2016 which is history is any guide, ought to mean another dozen of so operating assets added to the mix. The point of the exercise here is to look forward and realize by 2017, the company is going to have a problem. What to do with the $200m-$300M /yr the operating assets are now generating (plus income from the closing of sales at the Hawaii towers). Since we can assume Ackman as Chairman will have a say and being the Buffett devote he is, I highly doubt a dividend will be in order. The most likely scenario is a large buyback or acquisitions.

Remember, this is a highly unlevered company so the flexibility they will have with the balance sheet for either or both options will be extraordinary. REIT conversion? I have spoken in the past about this and while I do think at some point it will make sense, given the NOL’s they have to work through, the property specific debt that will reduce profits (taxes) and the depreciation on newer assets, while the company will be fundamentally operating at a high level and generating gobs of cash, accounting will enable them to maintain the assets within the C Corp structure for a few more years to maximize their specific tax attributes.

There is a major difference between the way $HHC operates and other land rich companies have in the past. Historically other companies have sold their land to developers and the only income they generated was from land sales. $HHC has taken a different tact. They are using residential land sales to build operating assets within those communities that will generate recurring income for years. Further, where applicable they are simply providing the developer the land for a project in return for a 50% interest in it. Here are a few of the many deals like this they have done:

Summerlin Apartments, LLC

On January 24, 2014, we entered into a joint venture with a national multi-family real estate developer, The Calida Group (“Calida”), to construct, own and operate a 124-unit gated luxury apartment development. We and our partner each own 50% of the venture, and unanimous consent of the partners is required for all major decisions. This project represents the first residential development in Summerlin’s 400-acre downtown and is located within walking distance of downtown Summerlin. We will contribute a 5.5-acre parcel of land with an agreed value of $3.2 million in exchange for a 50% interest in the venture when construction financing closes. Our partner will contribute cash for their 50% interest, act as the development manager, fund all pre-development activities, obtain construction financing and provide any guarantees required by the lender. Upon a sale of the property, we are entitled to 100% of the proceeds in excess of an amount determined by applying a 7.0% capitalization rate to NOI. The venture is expected to begin construction in the fall of 2014 with a projected second quarter 2015 opening for the first phase and the final phase being opened by the end of 2015.

Millennium Woodlands Phase II, LLC

On May 14, 2012, we entered into a joint venture, Millennium Woodlands Phase II, LLC (“Millennium Phase II”), with The Dinerstein Companies, the same joint venture partner in the Millennium Waterway Apartments I project, for the construction of a new 314-unit Class A multi-family complex in The Woodlands Town Center. Our partner is the managing member of Millennium Phase II. As the managing member, our partner controls, directs, manages and administers the affairs of Millennium Phase II. On July 5, 2012, Millennium Phase II was capitalized by our contribution of 4.8 acres of land valued at $15.5 million to the joint venture, our partner’s contribution of $3.0 million in cash and a construction loan in the amount of $37.7 million which is guaranteed by our partner. The development of Millennium Phase II further expands our multi-family portfolio in The Woodlands Town Center.

Parcel C

On October 4, 2013, we entered into a joint venture agreement with a local developer, Kettler, Inc. (“Kettler”), to construct a 437-unit, Class A apartment building with 31,000 square feet of ground floor retail on Parcel C in downtown Columbia, Maryland. We contributed approximately five acres of land having an approximate book value of $4.0 million to the joint venture. Our land was valued at $23.4 million or $53,500 per constructed unit. When the venture closes on the construction loan and upon completion of certain other conditions, including obtaining completed site development and construction plans and an approved project budget, our partner will be required to contribute cash to the venture.

So, rather than simply selling land, they are using that one-off sale of land to create assets that will provide shareholders recurring income into the future. Think about it. They have room for 40k more homes in Summerlin. Some of that I presume eventually they may build themselves, the rest they slowly sell to developers who then build the homes to grow the population to feed the massive Downtown Summerlin project. To do a little “how much” math on this, for the first 6months of 2014 they have sold 481 sites in Summerlin (that includes superpad, custom lots and SF detached lots) for an average price of $133k per site. Some simple cocktail napkin math says the remaining 39,500 sites generate in excess of $5B in sales. Of course this assumes no price increases over the next couple decades (reminder, Vegas is landlocked by mountains and HHC is the largest private landowner, there really isn’t “more land” for people to go build on). To show how this works the price per site in 2014 of $133k is just a bit above the $68k in 2013 (please note the sarcasm).

The financial strength of HHC and its strategy allow them the trickle out site sales to maximize price. Again, as an example the first 6 months of 2014 in Summerlin sales fell from 767 sites to 481 yet revenues in Summerlin rose $14M to $66M. In Bridgeland sites sales fell from 80 to 63 yet revenues rose $1.4M to $6.8M. I’ll note here Bridgland only just received approval from the Army Corps to build out the rest of the MPC (including retail) so they now have another 1,000 sites to sell there (they currently expect 429 lot sales in 2014). The Woodlands saw site sales fall (site prices rose to $156k vs $139k) but that is because they are simply running out of lots to sell and are concentrating on commercial there ($97M in sales vs $0 in 2013) to accommodate the Exxon campus. Don’t be worried about the Woodlands though, while they may be running out of SF lots to sell, I’d expect their mantra over the next few years there to be “go vertical” …..

This is company is going to be massive at some point. The best part about it is they are not going to have to lever up the balance sheet to get there. They can self fund a huge part of it via the avenues mentioned above leaving a company with spectacular flexibility to take advantage of any opportunities that may present themselves down the road (think buybacks).