“Davidson” submits:

There are 2 major man-made headwinds, the tight credit market and the excessively strong US$. The 1st arises from government entities that misunderstand how our economy works. The 2nd arises from Momentum Investors who misunderstood the outcome of the actions of the 1st. Both are likely to ease as we go forward, because we have always normalized credit and currencies over time. Either can impact the other although they are not related directly. As these headwinds begin to ease, we can expect a blossoming of optimism and higher equity prices in my estimate.

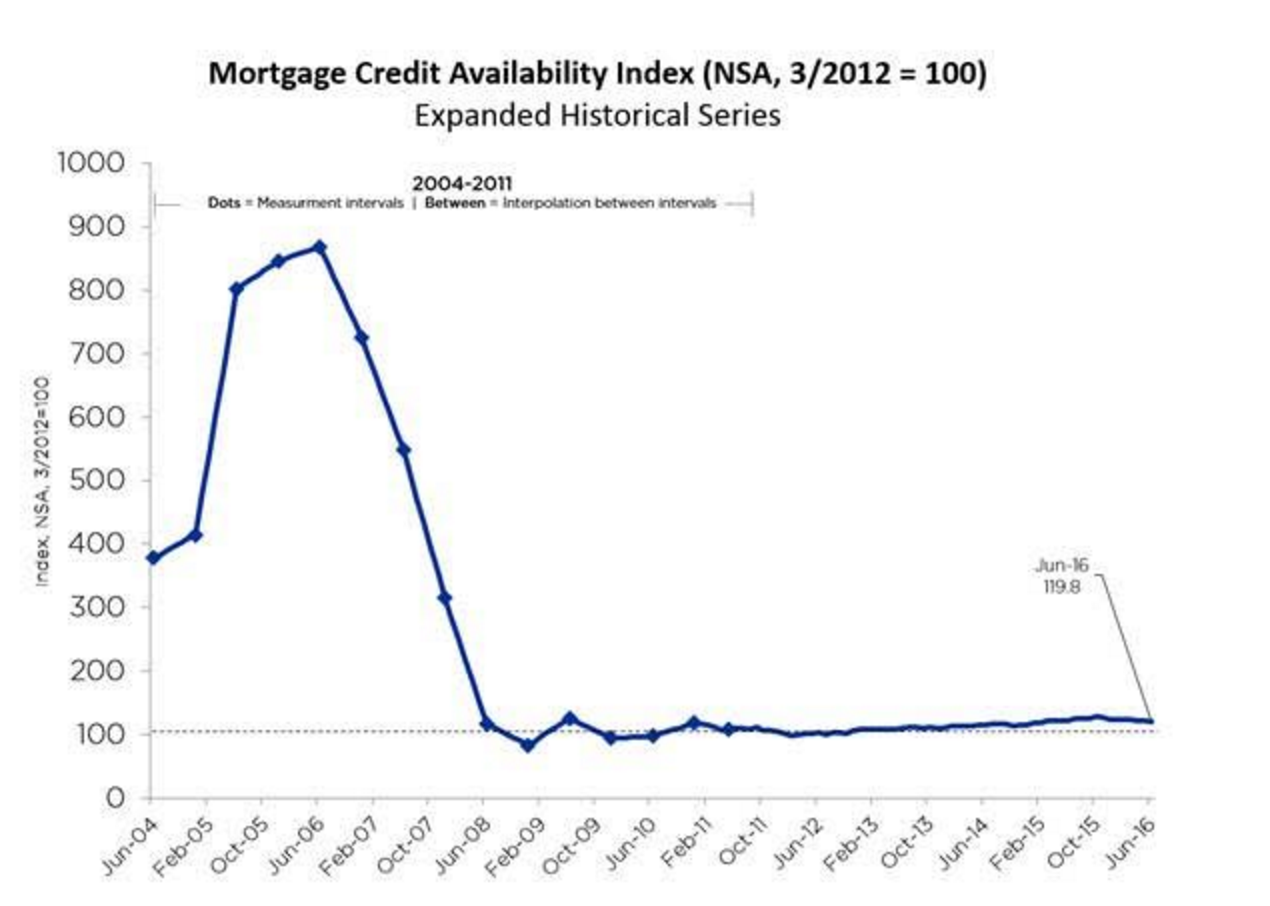

One of the reports I track is the MCAI(Mortgage Credit Availability Index). A feature of our current economy is a Fed which has forced 10yr rates below 2% with the belief that this is adding liquidity. It has not had this effect. Liquidity has always been correlated to credit spreads. Wider spreads produce higher Net Interest Income for lending institutions and encourages lending. For banks this means mortgage lending. The Fed is mistaken in believing that low 10yr rates will stimulate lending as can be seen by the MCAI(below). Credit conditions are very tight today in the mtg arena.

I take the MCAI June 2004 ~300-400 range as the quasi-normalized level of mtg lending before the rapid Sub-Prime expansion occurred in 2005-2007. Since then regulators have raised bank reserve ratios and added additional regulation. Then the Fed did OpTwist which forced 10yr rates lower and resulted in mtg lending at roughly 1/3 of what can be considered normal levels. In Dec 2015 the Fed raised the Fed Funds rate. Immediately the credit spreads narrowed and the MCAI has drifted lower. Today the US Single-Family Housing market is recovering at such a slow pace of mtg formation that we remain at the same level of yearly Single-Family Starts as we saw in the recession of 1991. We should be seeing upwards of 1.5mil S-F Starts. We remain below 800,000. Even with these headwinds, general employment, Real Personal Income and other economic measures are at record highs. The Fed does not understand banking very well in my opinion.

The Fed’s actions are on top of the Momentum Investor 2014-2015 shift in the US$ which has caused great disruption in the energy and Intl Trade sector. This trend is determined by long-term expansion of global trade relationships. I expect a reversal of the Fed’s mistaken liquidity actions. I expect that the US$ should normalize lower by ~30% to its historic trend. One cannot time these things even though one can see how the fundamentals work. The economic potential and investment opportunity is quite large in my opinion.

If we see even a partial reversal of both these headwinds, the economy should have a nice ramp-up. One cannot predict when we will see a reversal of these headwinds. History tells us that normalization away from extreme conditions always occurs.

There is no economic correction in sight precisely because household indebtedness is in very good shape and we continue to see debt pay down with mtg issuance at such a low pace.

This is how our economic environment looks to me at the moment. One has never been able to predict when these man-made headwinds ease, but take to heart that over time we adjust to long-term norms.

Mortgage Credit Availability Decreases in June

Jul 11, 2016 https://www.mba.org/2016-press-releases/july/mortgage-credit-availability-decreases-in-june