“Davidson” submits:

Markets are understandable if you think of them as part of our ‘Human System’. If one looks at the market empirically and not try to impose what you think should occur, one can see that prices are correlated to corporate financials and economic activity over the long-term. This means that buying and selling opportunities occur far less frequently than what many believe and promote in the media. Investing with economic and business fundamentals is called ‘Value Investing’. Trading the same security several times a year (or more often) due to minor changes in price makes little sense if one is a Value Investor because Value Investors know that actual value increases slowly with businesses operating in an economic cycle which may last more than 10yrs. If one can identify good companies, that is companies which are run by CEOs who follow ‘lean’ business principles, one often finds that the holding period is equivalent to the business cycle. The goal for Value Investors then is two-fold: 1) Identify those economic indicators which let one efficiently track the business cycle and 2) Identify those portfolio managers and company CEOs who create better value during the cycle.

Value Investor Approach:

1) Identify those economic indicators which let one efficiently track the business cycle

2) Identify those portfolio managers and company CEOs who create better value during the cycle.

3) Identify the price levels which represent under-value and over-value across the business cycle.

The Human System does not follow a mathematical formula. It is in a constant process of creative evolution which leaves the future always unknowable and at the same time better than the past. Our standard of living improves with our creativity. We operate businesses with ‘creative competition’. Businesses are formed to make profits by providing consumers with products and services which improve our standard of living. For products and services to be successful, consumers must find they provide better value than competing offerings. It is useful to think of consumer spending as directed towards those goods and services which bring improvements to one’s standard of living at the lowest cost. Those companies which offer the greatest intellectual contribution to improvements in our standard of living are rewarded with the highest profit margins.

Corporate success in delivering offerings which are attractive to consumers is reflected in Net Income Margins. It is helpful to think that the more value a company uniquely provides, the greater its Net Income Margins. A good way to understand this is by examining Apple’s creation of the Smartphone category of cell phones. Apple introduced its iPhone June 27, 2007. In 2007 this was and is still the most expensive smartphone offered. It was revolutionary in what it permitted consumers to do. Consumers suddenly found a device which let them connect with people and information systems incredibly conveniently and on the run while doing other things. Up to this point consumers were overloaded taking on the multi-tasking required for modern life which was made difficult with limited access to the information, calendars and communications on which they had come to rely. Apple’s iPhone was an elegant solution. It streamlined multi-tasking leaving time for consumers to satisfy much needed personal time. Now most consumers have smart phones. Apple’s success at meeting consumers’ needs was reflected in its Net Income Margins widening to ~26% in 2012. Since then, competitors have begun to catch up and Apple’s dominant market share has fallen as has its Net Income Margins.

Apple’s Net Income Margins*:

2006-09 2007-09 2008-09 2009-09 2010-09 2011-09 2012-09 2013-09 2014-09 2015-09 TTM Net Margin % 10.3 14.56 14.88 19.19 21.48 23.95 26.67 21.67 21.61 22.85 21.7 Revenue USD Mil 19,315 24,006 32,479 42,905 65,225 108,249 156,508 170,910 182,795 233,715 220,288

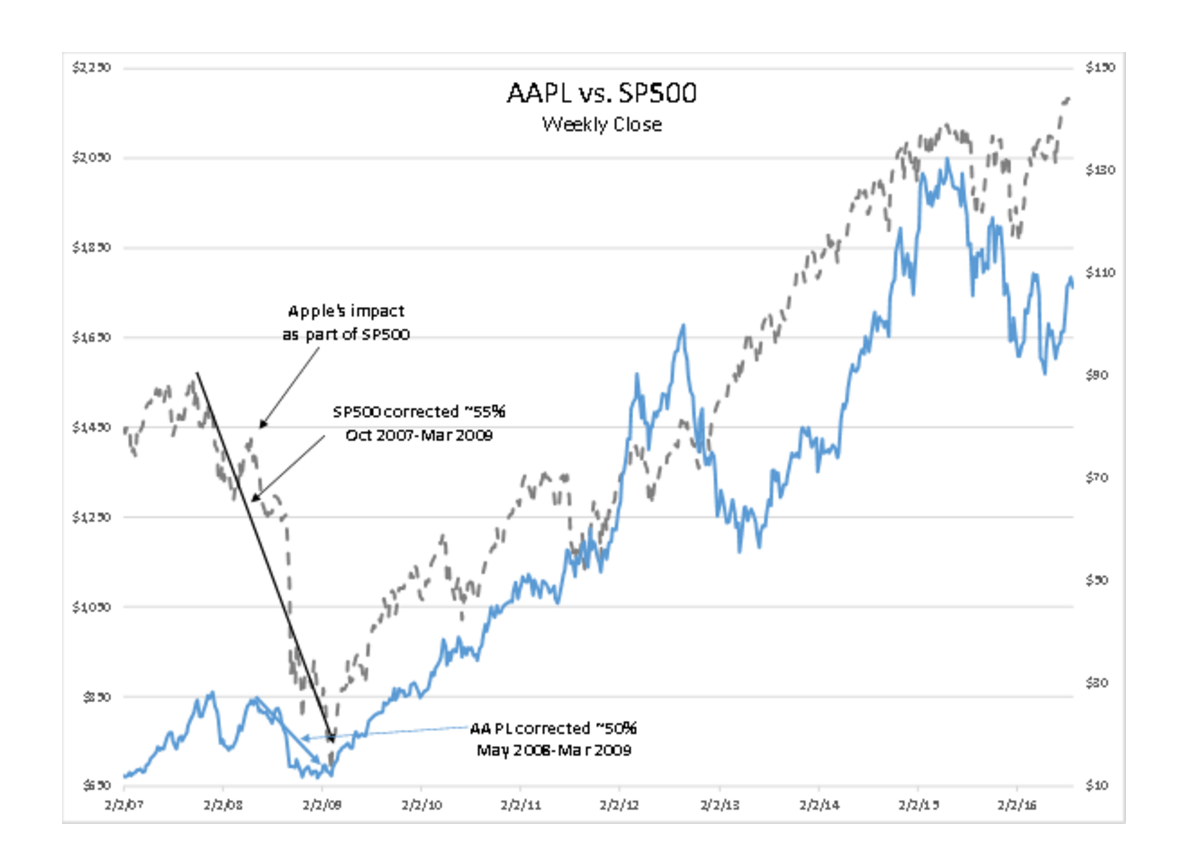

Apple’s iPhone introduction dominated the Smartphone market early on. Its widening Net Income Margins and expanding revenue resulted in its stock price holding up for most of 2008-2009’s market correction. It finally succumbed to Hedge Fund selling. Notice that the SP500 has multiple price shifts in line with those in AAPL. The SP500 is a market cap weighted index and as AAPL has grown relative to other SP500 constituents, AAPL has had an increasing impact on SP500 pricing. Beginning May 2015 AAPL has declined as revenue slows and Net Income Margins decline, but other SP500 constituents have risen. Market indices can come to be dominated by single issues and sectors which distorts short-term performance analysis. One should never benchmark a portfolio over short periods of time.

Apple’s iPhone and Net Income Margins continued to dominate markets till 2012. After 2012 Steve Jobs’ product innovations ended with his passing. According to statista.com Apple’s Smartphone share peaked at 23% in 2012 and now holds ~11% share. http://www.statista.com/statistics/216459/global-market-share-of-apple-iphone/

Steve Jobs impact on Apple’s financial performance and consequently it stock performance is not unique. Bill Gates as CEO of Microsoft likewise offered a software package which permitted users to greatly simplify and efficiently process information for a host of analytical purposes. It has become known as the Microsoft Office Suite. The Net Income Margins were similar to Apple’s because its value to consumers was similar.

Microsoft’s Net Income Margins*:

2007-06 2008-06 2009-06 2010-06 2011-06 2012-06 2013-06 2014-06 2015-06 2016-06 TTM Net Margin % 27.51 29.26 24.93 30.02 33.1 23.03 28.08 25.42 13.03 19.69 19.69

Contrast these margins with Net Income Margins of Wal-Mart(discount goods distributor*:

Profitability 2007-01 2008-01 2009-01 2010-01 2011-01 2012-01 2013-01 2014-01 2015-01 2016-01 TTM Net Margin % 3.24 3.36 3.3 3.51 3.89 3.51 3.62 3.36 3.37 3.05 2.99 …or Net Income Margins of Kroger(food distributor)*:

2007-01 2008-01 2009-01 2010-01 2011-01 2012-01 2013-01 2014-01 2015-01 2016-01 TTM Net Margin % 1.69 1.68 1.64 0.09 1.36 0.67 1.55 1.54 1.59 1.86 1.89

Those companies which offer the greatest intellectual value to improve our standard of living are given the widest Net Income Margins by consumers. For distributors of others’ products which provide little added value to consumers. Net Income Margins are much less for discount retail stores and grocery stores. Net Income Margins are a good general measure of the intellectual value corporations add to society’s standard of living in my opinion.

*Morningstar data

The Take-Away:

1) Individuals create value and seek to profit in a competitive marketplace. They convert intellectual value into marketable products and services.

2) Consumers decide which products and services add value to their standard of living and decide which products will succeed in the marketplace.

3) Those companies which offer the greatest value to consumers have the widest Net Income Margins.

4) Companies must be managed by competent CEOs if they are to continuously succeed with consumers.

The Value Investor Perspective:

Only a few examples are provided here of the relatively wide range of business returns. The markets make investing complex by the fact that investor perceptions price each of these issues relative to future expectations of general economic, sector and individual corporate financial performance. Value Investors make their investment decisions based on a stock’s price and the financial performance of the CEO. Value Investors know that the ultimate performance of any corporation is not from its products, but derives from the decisions of the CEO. If one identifies an exceptional CEO, Value Investors frequently buy shares during periods of market distress with commentary about how skilled is the CEO. Value Investors in effect buy the CEO’s financial performance at cheap prices even though they talk about historical Book Value and Cash Flow. After all, companies do not self-assemble to make offerings for consumers. Companies are assembled and operated by people with creative ideas. It requires a competent CEO for a company to continuously succeed with consumers who are the ultimate decision makers of corporate profitability. The CEO is the focus of the Value Investor.

Companies do not self-assemble to make offerings for consumers. Companies are assembled and operated by individuals with creative ideas. It requires a competent CEO for a company to continuously succeed with consumers who are the ultimate decision makers of corporate profitability.

Thinking about markets as something which is evolving with society’s advances, a ‘Human System’, is not a traditional approach, but it is the only way to approach making sense of how we as a society convert our creative energy into corporate activity, advance our standard of living and put a price on what we think things are worth at various points in an investment cycle. We are forever in a system of competitive invention seeking cheaper, faster and improved means to bring greater value to consumers. Predicting specific invention and discovery is impossible. Being able to see how we generally do this, which companies do it better than others and understanding how they come to make this part of their corporate culture is something we can do. Doing this requires the Empirical Method. The empirical approach is to simply observe how fundamentals correlate with market prices and couple observations to how Value Investors think differently than Momentum Investors. When one does this, it explains the diversity of pricing very simply.

Applied to investment markets the Empirical Method finds that only longer term financial trends correlate with market prices. Economic and individual financial rends are simple to observe over years. The correlations to investment cycles, to investment sectors and even individual stocks is not hard to visualize.. It becomes a matter of identifying the better long-term managed companies and then taking positions in them when markets have priced them low relative to their long-term value creation. Value Investors do this and are comfortable holding through periods of temporary market volatility because they are monitoring fundamentals. Value Investors are not know as traders. Momentum Investors do not use fundamentals. They rely solely on tracking price trends and trade frequently. Some Momentum Investors trade the same issue multiple times in a single day. The media in its market reporting by sheer level of activity focuses mostly on the activity of Momentum Investors whose views can vary widely week to week. What the average investor hears is very confusing. The long term view is far more simple to understand.

Today’s Perspective:

I am a Value Investor who understands Momentum Investors. Momentum Investors are calling a market top. The fundamentals do not support this thinking. Economic activity globally continues to expand. One can see severe imbalances in US$ being 30% over-valued historically and 10yr Treasuries at 1.6% as being grossly over-priced. These two imbalances are connected by fears of deflation and slowing economic activity for which we have no evidence. It remains a distinct possibility that when the quantity of capital which created these imbalances begins to normalize towards long-term fundamental economic trends, equity markets here and internationally could rise markedly.

The advantage for Value Investors today is that we see economic growth when most do not. Eventually, capital chases economic returns. This has always occurred in our history. I expect it to occur yet again.