“Davidson” submits:

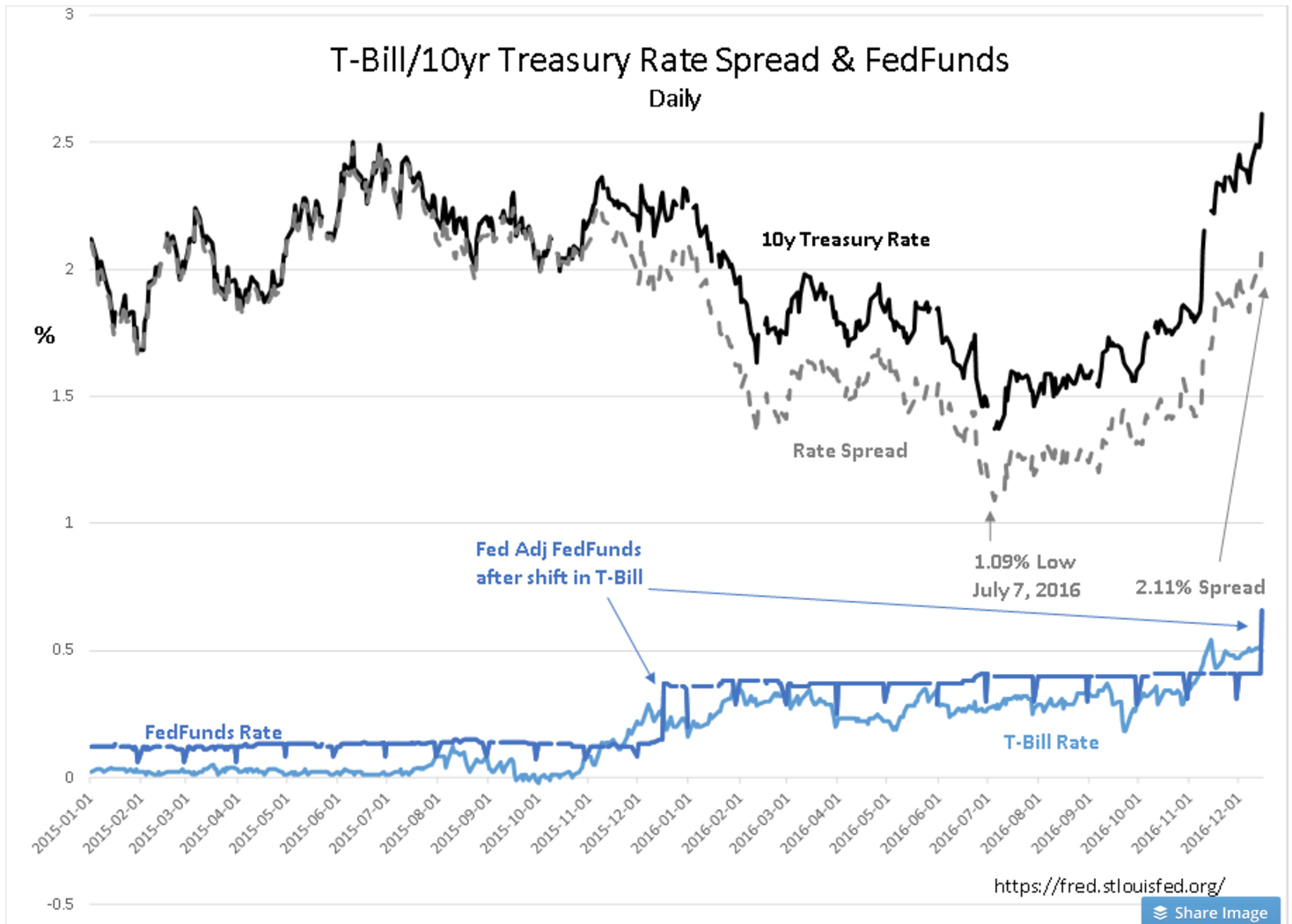

Some ideas remain market lore because so many in the rush to adjust investments in the context of long-held beliefs do so simply because they do not believe one can do otherwise. That the Fed controls interest rates is one of these beliefs. The mystery behind Fed rises in the Fed Funds rate has been a market focus for many decades. The data comprising Fed Funds, T-Bill and 10yr Treasury rates tells a far different story. Fed Funds rate is adjusted to fit shifts in T-Bill rates. The only exceptions to this pattern occurred when Chairman Volcker acted unilaterally to quash run-away inflation in the early 1980s. If one examines the daily data available, there will be seen that there is no doubt that the Fed moves only after T-Bills have shifted in response to market forces.

The Fed responds after the fact to T-Bill rate shifts to keep the Fed Funds rate higher. Chairman Volcker, once he had put an end to the 1970’s inflation-spurred consumer spending psychology, kept Fed Funds ~1.00% higher than T-Bill rates with a 1mo-3mo lag. Chairman Greenspan did the same with Fed Funds ~0.40% higher as did Chairman Bernanke. It appears that Chairperson Yellen is tracking T-Bill rates with Fed Funds ~0.25% higher. Recent Fed Funds adjustments support this observation.

I think it is unfortunate that markets are constantly surprised by Fed Funds rate adjustments. Many believe that the Fed controls our economy when the Fed actually has little influence beyond setting bank capital levels and regulations. The Fed no more causes economic peaks with higher rates than they spur economic recovery with lower rates. Rates are set by market behavior within rules set by Congress and the Fed seeking to keep lending within prudent guidelines. Historical data provides considerable guidance months and even years ahead. I think it is unfortunate when most investors make decisions based on myths for which there is no historical evidence. The Fed does not control rates. Rates are set by millions of individual spending and investment decisions. Rates are controlled by you and I. Nonetheless, markets are human systems and strongly influenced by market psychology of what things are worth and perceptions of what they are likely to be worth months and years ahead.

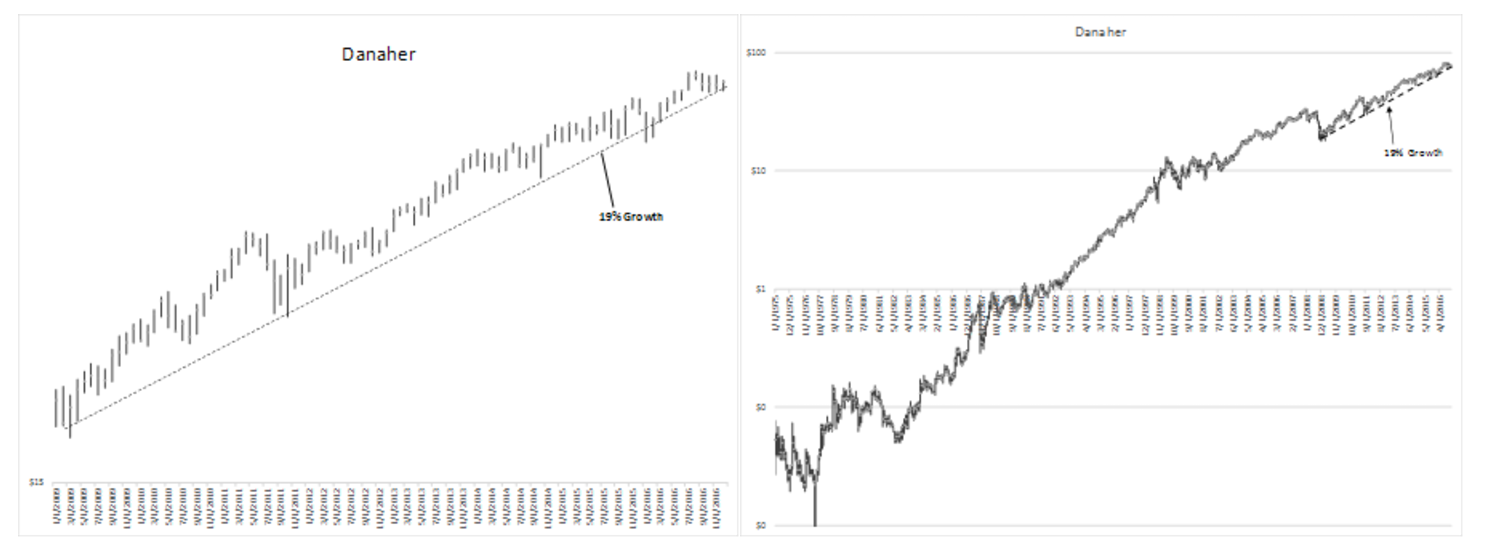

If we have an environment favoring bank lending, then bank lending expands resulting in economic expansion. The widening spread between T-Bills/10yr Treasury favors expansion of bank lending and economic activity. This spread has widened from the July 2016 1.09% level to 2.11% this morning. It expands as investors shift capital to areas though to offer better returns. For investors it is more productive to identify corporate cultures which have the skills to take advantage of economic expansion rather than spend the effort to identify sectors, industries and countries. I focus on identifying highly skilled management and invest when I think the pricing is favorable. Over time, one can build a naturally diversified and portfolio of well managed companies. Danaher is a good example of a well managed company.

Danaher(DHR) is the ‘poster child’ of ‘lean business practices’ in the US. Their specific approach, driven by Steven and Mitch Rales, began with Art Byrne in 1985 and is the American version of the famous Toyota Business System(TBS). Many Danaher trained managers have left the company since the early 1990’s to develop similar ‘lean’ practices throughout US corporations. ‘Lean’ is now practiced at Ford, GE, United Technology, Medtronics, EOG and many smaller companies. ‘Lean’ is what keeps US corporations globally competitive. Bringing ‘lean’ into an underperforming situation can have dramatic positive impact on the stock price. Fundamental to ‘lean’ is a focus by every employee on meeting customer needs with every employee sharing in the profits of the company. When management learns and applies this approach, corporations have significantly improved financial performance over time which investors price into the company’s shares. Gross Margins, Operating Margins and Net Income % as shown in DHR’s Morningstar data reflect improving trends which one sees with ‘lean’ management The shares reflect investor confidence.

DHR’s share price represents management’s success.. The TTM(Trailing Twelve Month) Operating Margins at 17.5% represent the highest in the past 11yrs. DHR’s lower earnings come from recent acquisitions, the expenses involved in the Fortive spinoff and currency translation issues due to the strong US$. I estimate that each of these are temporary situations and the long-term rise in Net Income % is likely in the next 12mos. I own this issue personally as well as the spinoff Fortive(FTV) and a relatively new company Colfax(CFX) formed by the Rales brothers in mid-1990s and IPO’ed in 2008.

Danaher has a record useful as an example to explain the concept of a good corporate culture. Fortunately, there are many to choose from. It is these well managed companies which one uses to take advantage of periods when there is economic expansion. Every company is priced differently dependent on market psychology. There is only one rule of thumb. If the corporate performance continues at its historical pace, the shares are likely to be priced as they have historically. But, investors must always be aware that market psychology changes with the perception of corporate growth. If market psychology is more pessimistic than actual corporate performance justifies, then Value Investors see a buying situation and vice versa. Investors must at all times be able to judge how market psychology correlates to corporate performance.

As long as economic expansion continues, one can buy any well run corporation. The key element is the quality of the management team. Economic expansion is like an incoming tide. All ships rise. The better managements will get the better returns on capital. One’s focus, once it has been established the economy is expanding, is to make sure one has identified a good price for the shares.

If you have done this for 100+ decent companies, you get a good sense of the overall economic environment and marketplace.