“Davidson” submits:

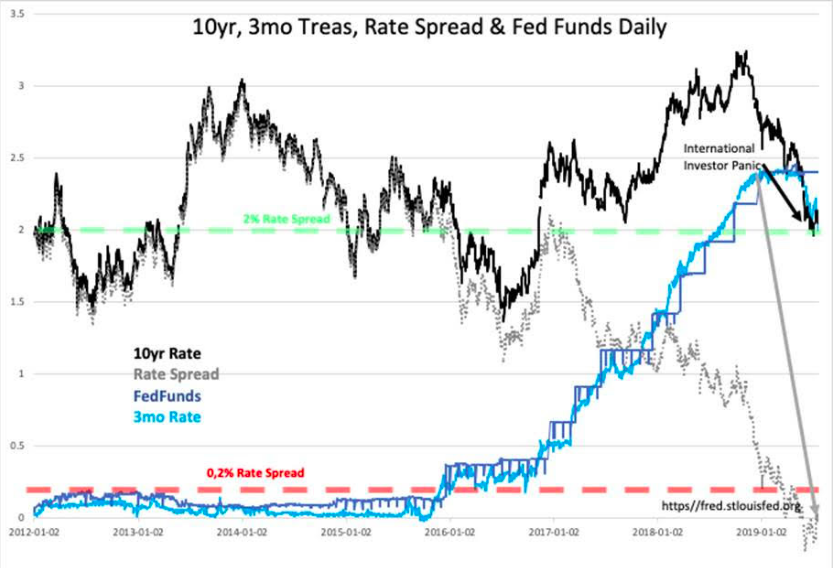

The interest rate chart of 10yr, 3mo Treas, Rate Spread & Fed Funds Daily shows the current Fed policy of raising FFunds rate to equal T-Bill rates after T-Bill rates rose about 25bps(0.25%). This deviated from 70yrs of Fed history of keeping FFund rates higher than the T-Bill rates(a market set rate) to discourage firms seeking to actually borrow from the ‘Fed Funds Window’. With Chair Powell this has decidedly taken a different tack. Historically the Fed has adjusted FFunds after T-Bill rates shifted with market forces.

Today, T-Bill rates have fallen to 1.99% while FFunds remain at 2.4%, a 41bps differential. The Fed could lower rates by its typical 25bps to 2.15% or simply wait and see if economic weakness which all seem to be predicting occurs and act once the economic direction has become better defined.

In my opinion, the Fed will do nothing at the moment and take a wait-and-see stance. The economic expansion remains on trend to date with little signs of slowing. Should the Fed act with this short-term shift in T-Bill rates they would lose credibility should rates suddenly rise as investors jump back into equities with most 2Q19 reports already being better than anticipated.

Today’s US$ denominated debt markets have significant inflows from other currencies which have greatly skewed the historical rate relationships used by some to signal an economic slowdown. Algorithms have helped panic investors on these signals with sharp equity sell-offs even in the face of record earnings reports. If Powell is tuned to all the data available, he will keep FFunds unchanged till something more than an inverted yield curve signals economic weakness. Powell is likely to keep rates stable till employment, personal income or retail sales, which are currently still signaling economic expansion, provide a more comprehensive economic signal that he should follow the direction of market rates.