“Davidson” submits:

Highlights: US Crude Inventories 25.7mil BBL below 5yr mov avg. Tied to algorithms and believed to be a sign of economic strength/weakness, current trend suggest a marked shift to positive market psychology. Economic strength has continued on trend since 2009 with the past 20mos of pessimism unjustified.

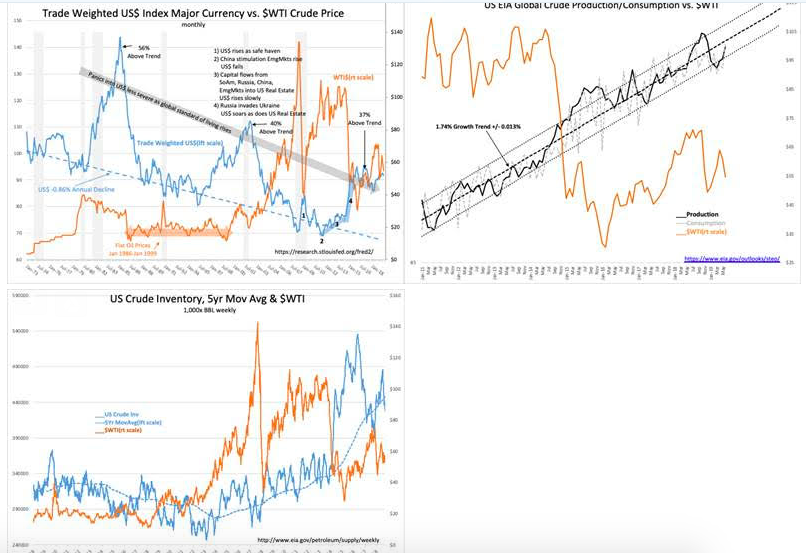

No two market cycles are identical. We see that this time a strong US$ is the response to autocratic government threats to native capital has driven that capital to Western markets especially so to the US. The US/China tariff initiatives have accelerated capital out of China driving the Yuan lower, the US$ higher, real estate prices higher and 10yr Treasury rates lower. This is a combination not witnessed in previous market cycles. Trading algorithms are also a relatively new presence relying on past price patterns correlated to rates, the US$ and oil prices which are believed to telegraph changes in investment opportunities. Traders use algorithms to be first to see changes in market trends to maximize returns. Part of this coupling of signals together to be first incudes oil prices as an economic indicator. Higher oil prices are related to higher demand by economic expansion and vice versa. Past cycles have witnessed certain price patterns which provide the confidence to correlate or inversely-correlate specific price trends. With $Trillions under management and using ETFs, the periods of daily volatility make one’s head spin. More so when positive quarterly reports are met with plunging equity prices eliminating expectations that markets operate with commonsense. The fact is that markets do indeed track economic data, but one may have to wait 12mos+ for market psychology to catchup to underlying economic dynamics.

The past 24mos (beginning Oct 2018) has seen a dramatic rise of investor pessimism well out of sync with underlying economics. This has been due to algorithms reliance on certain measures which in turn has acerbated other measures. It began with capital shifting to the US$ which drove 10yr Treasury rates low enough to invert the yield curve, a major signal for algorithms. Algorithms then sold oil prices lower to offset expected recession related declines in equities. The belief that oil Supply/Demand swings wildly during economic ebbs and flows is what drives oil prices-see Trade Weighted US$ Index Major Currency vs. $WTI Crude Price. In fact, oil prices have volatility not related to Supply/Demand which has been growing ~1.74% annually with minor volatility from this trend of 0.013%. That is, Supply/Demand does not vary much at all from the 10yr trend-see US EIA Global Crude Production/Consumption vs. $WTI.

Where the correlation of $WTI does come into dramatic focus is US Crude Inventories vs. Inv 5yr mov avg-see US Crude Inventory vs. 5yr Mov Avg & $WTI. The correlation of periods of higher/lower $WTI is pronounced to periods when current US crude inventories are lower/higher than its 5yr mov avg. Higher/lower $WTI does impact the cash flows and the pace of business for energy related businesses. However, in the current cycle 2009-Present, the economic pessimism which developed in 2014-2016 with the drop in $WTI did not produce a recession. The US economy continued to expand and even accelerated somewhat with tax cuts and reduced regulation. So strong is the belief of the coupling of low oil prices to gross economic trends that once the yield curve inverted Oct 2018, $WTI plunged 40% and a persistent fear developed of a major recession which lasts even today.

Hmm…conditions appear to be on the verge of turning market psychology more positive. US Crude Inventories persisted above normal Spring 2019 with multiple refinery outages and upgrades. This activity resulted in a fall in US Gasoline Inventories well below seasonal needs. Only recently have refineries come back on line. The result has been a drop in US Crude Inv ~25.7mil BBL below the 5yr mov avg. If crude inventories persist below the 5yr mov avg and traders take this as a sign of positive economic activity, then the pall of recession should lift and all equity prices should benefit.

Making predictions of changes in market psychology is always an educated guess based on hindsight and whether current market psychology reflects current economic trends. Overly pessimistic market expectations can prove explosive to prices should investors turn positive at once. My guess is that markets could turn higher fairly quickly.

To access member-only content with a 5 day FREE trial follow this link and enter code “VP30” for a 30% discount