“Davidson” submits:

The US$ exchange rate has trade and investment flows. Shorter-term fluctuations can be tied to geopolitical impacts as individuals adjust capital to perceived risk/return. Longer-term includes trade flows and in my opinion the impact of Modern Portfolio Theory(MPT).

MPT is a mechanical capital allocation tool developed in the early 1950s to remove human emotion from investment decision making. Harry Markowitz received a Nobel Prize in 1990 in part for MPT. In 1985, Charles Ellis published his classic on MPT, “Investment Policy: How to Win the Loser’s Game”. Today, every financial institution offers Financial Planning or ‘MPT simplified’ as an offering to manage individual investor assets cheaply and describe it as having long-term “predictable outcomes”. In my estimation, MPT over-simplifies to such a degree that it exposes investors to significantly poorer risk/return outcomes. This is the opposite of what many have been taught.

The basis of MPT is statistical analysis of market prices. From this emerges index performances and index volatility. The basic and simplistic assumptions are that the higher the growth of a company, the higher the quarter to quarter volatility of its price. The process of investing requires identifying and determining the statistical characteristics of asset classes, allocate to a volatility/return benchmark desired and rebalance back to that allocation on a mechanical schedule. The goal is to keep human emotions out of the process and in Ellis’ belief “…win the loser’s game”. It sounds simple enough! Sounds fool-proof! What could go wrong?

What could go wrong is the basic assumption that markets which reflect evolutionary changes in human thinking over time cannot and never have been modeled by mathematics. To those whose main tool is mathematics, they tend to seek answers to everything as operating by a mathematical analog. This is simple to teach. The alternative requires an in depth review of changes in societal perceptions over centuries, changes in our self-governance and rule making and some economic insight that helps to identify misperception from factual outcomes. It requires continuous review of what has been assumed as new facts come to one’s attention to sharpen one’s foresight by resetting one’s hindsight as one moves forward. This has a level of complexity that is only learned through years of experience and cannot be taught at even the finest educational institution. What MPT misses completely is the impact of geopolitics on global capital shifts i.e., how people think of their savings and investment in response to threats.

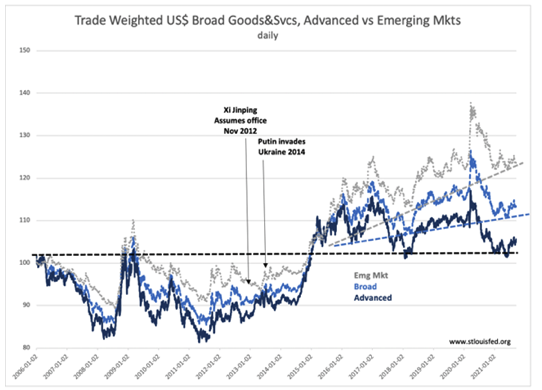

The Trade Weighted US$ Broad Goods&Svcs, Advanced vs Emerging Mkts provides a good example regarding the issues to which investors are exposed using MPT. This chart notes Xi becoming President of China and Putin invading Ukraine. In 2014 Erdoğan, became President of Turkey. These are just 3 of shifts towards autocratic governance and threats to local property protections. There began a notable shift strengthening the US$ beginning 2012 representing the rise of these individuals and others to autocratic governance globally. It is by connecting geopolitical shifts to exchange rates that it become obvious that capital has been shifting towards Western markets as a safe haven for some time. The result has been a pooling of capital in Western Sovereign Debt forcing German and Switzerland 10yr to negative rates to the consternation and confusion in those following MPT who did not and still do not perceive the impact autocratic governance has on capital in an ever more globally connected financial system. The same pricing impact has occurred with Western real estate which is another preferred asset class of investors exiting EmgMkts.

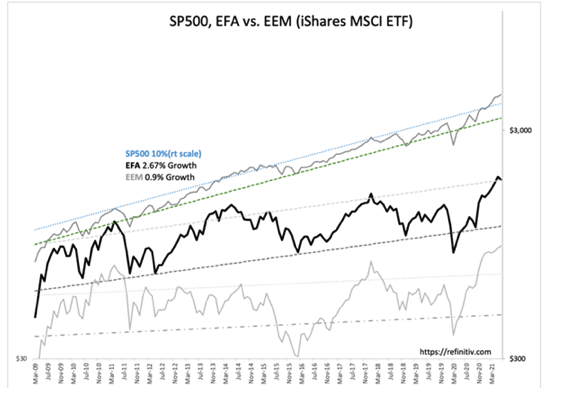

What compounds the impact of MPT is the underlying assumption that smaller = higher returns. It is this assumption which has caused Western portfolio managers to open up EmgMkts providing development capital and liquefying formally illiquid opportunities in the desire to achieve higher returns. After an initial period of performance, it is clear from SP500, EFA Vs. EEM that the promise of higher returns has received a dismal response. The issue can be explained in the relative US$ strength of Advanced vs Emerging Mkts. A stronger US$ relative to Emerging Mkts tells us that capital put into those markets is being recycled back to Western sources, specially so it is being shifted to the US$. It is human behavior to seek a safer return of one’s life savings if the opportunity presents.

Bringing together the perspective of exchange rates, the impact of autocratic governance, the declines in Sovereign Debt rates/rise in real estate prices, one recognizes that following MPT, as many do with it being infused into portfolios as Financial Planning, placing funds into EmgMkts is detrimental to one’s portfolio. Yet, the current advice remains that investors allocate up to 40% to EmgMkt assets to offset the low rates experienced in the 30%+ recommendation for historic low returns in fixed income exposure. That MPT in the guise of Financial Planning provides identical investment advice to every investor is a recipe for portfolio destruction at some point. It certainly is not helping returns currently.

The recommendation for investors continues to be, with the current economic conditions, the primary portfolio focus should be US markets. This advice differs greatly from what is commonly advised today, but the evidence strongly supports this stance in my opinion. As we see the business/market cycle evolve, we should be prepared to adjust proactively. Economic/market trends adjust slowly. History provides enough of a signal, a yield curve inversion carrying specific patterns in my experience, that there has always proved enough time to adjust prior to the next major decline. At the moment, remain invested, be selective, be patient and let the returns build. This cycle still has 3yrs-5yrs to run.