Davidson makes a salient point here. Recessions typically come about as a way to work of excesses in the economy. I think it would hard to argue there are many excesses now. Of course it depends on how one defines “excess”. One can take any level marginally above historical levels and call it “excess”. Personally. I am of the thinking “excess” involves not quite a bubble (there are none of any significance out there now) but froth in several areas of the economy. Perhaps in small sectors there is some now but they are not of significance to cause a recession.

“Davidson” submits:

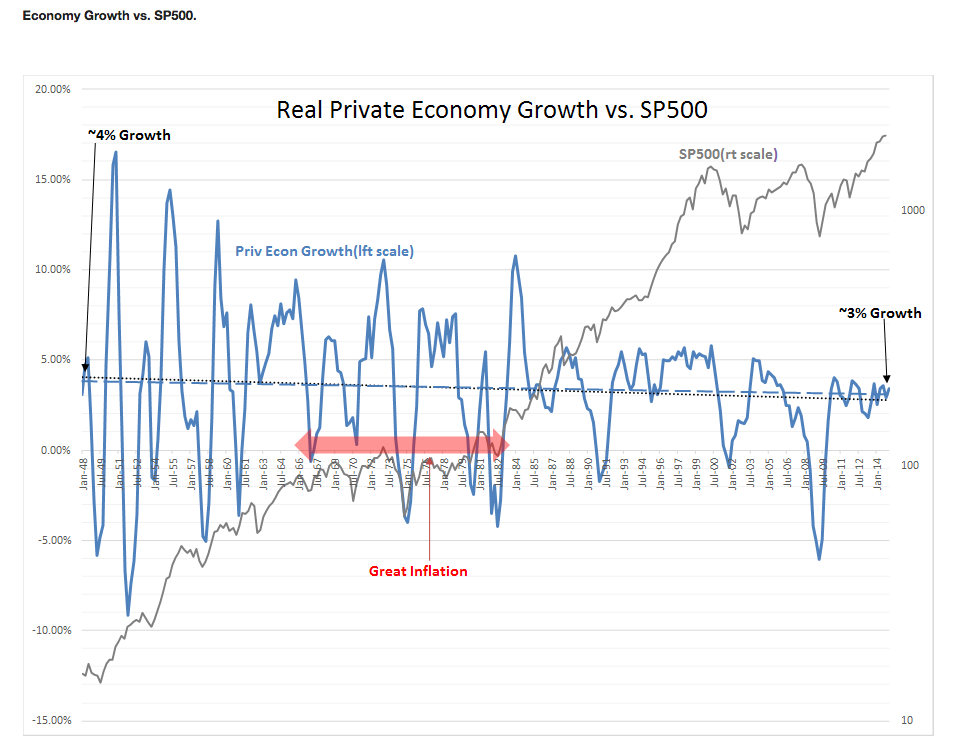

Value Investors learn lessons from our past. They learn to be optimists. They are long term investors because they have studied human economic activity as far back as several thousand years. Markets cycle with economic activity. This is true even with every cycle having its unique features. The same is true today of our economy as shown in the chart Real Private Economy Growth vs. SP500.

1) For the US there is a long term Real Private Economic growth rate trend about which cycles occur, DASHED BLUE LINE. Knut Wicksell called this the “Natural Rate” in 1898. It is dependent on the political/legal structure of one’s economy or in short the rules of self-governance. (Priv Econ = Real GDP – Govt Expenditure&Investment)

2) The rules we live by can be changed and result in different economic outcomes. A good example of rule change and outcome is what has occurred in Venezuela. Venezuela was considered economically vibrant in the 1990s. Since it embraced Socialism under Hugo Chavez in 1999. fuel, water, electricity, food and certainly individual freedom have become scarce as socialism forced new standards on the populace. Venezuela’s GDP has collapsed, inflation is raging and the government is expected to default on its debt in the next few months. This as taken ~15yrs which is a pattern witnessed in the US attempts at social engineering. The ‘Great Society’, Vietnam War and ‘Man on the Moon’ programs resulted in the ‘Great Inflation’. The chart shows the impact inflation has on market valuation. From 1965 to 1982, market response to economic cycles was subdued as inflation reduced the values of returns to Value Investors. Once Paul Volcker acted to reverse the nation’s inflation, markets reflected greater sensitivity to economic cycles and valuations expanded with disinflation.

3) Looking closely one can see that periods of excess growth of ~2% above trend are always followed by corrections. The period of excess can be a couple of years or it can be longer. There is no ‘timing rule’ for a correction after a period of excess. Higher economic growth has always been reflected in higher equity markets and vice versa when inflation remained steady.

4) How markets perform is important. If inflation rises with growth, Value Investors are less willing to pay higher market prices. If inflation falls with growth, Value Investors are willing to pay higher market prices.

Value Investors do not confuse fundamental returns with market pricing. Value Investors are sensitive to the translation of fundamental returns in market prices. “Value is what you get, Price is what you pay!” is the lesson Warren Buffett says he received from Ben Graham.

Real Private Economy = Fundamental Return

Market Pricing = Investor Perception

The argument many Macro-Momentum Investors present today is that 7yrs of economic expansion is the limit to economic growth as if there is a rigid timeline to economic activity. There are in fact no rules to economic growth but one, i.e. let there be a ‘Free Market’. Make access to economic opportunity ‘fair’ and ‘available’ to all and let individuals decide for themselves which goods and services they purchase, permit a competitive marketplace for goods and services, i.e. a Free Market, and economic activity will grow with little inflation at its highest pace. If we go to excess, we correct so that the inherent ‘Natural Rate’ of our economic system as we govern it averages to trend. The ‘Free Market’ is not permission to do act in any way one wants to as many seem to describe it when they want to change ‘outcomes’. The ‘Free Market’ permits wide freedom of choice in a market-based-decisions environment within clear guidelines to ensure fairness to all. That each of us has different abilities and that society may value those abilities differently results in different outcomes. It is individuals seeking the best value for their income among competitively priced offerings which creates economic vibrancy. All of us act in one fashion or another as consumers and producers. The US is the best model at the moment for the ‘Free Market’. Even here, we periodically confuse ‘equal opportunity’ with ‘equal outcome’. The ‘Great Society” attempt at large-scale social engineering, similar to Venezuela, created an uncompetitive marketplace and ‘Great Inflation’ was the result. Government domination of economic outcomes has never proven viable. The argument between those who desire ‘equal opportunity’ vs. those who desire ‘equal outcome’ has raged for a long time. Hamilton and Jefferson argued the same in creating the US Constitution and the meaning of our Declaration of Independence.

Economic activity is based on the rules we impose on our ‘human system’. We constantly seek ‘fairness’. The ‘Free Market’ with ‘strong fairness rules’ provides the best outcome. We often fail to see this.

In our current economy we have placed constraints on banks lending to home buyers. We blame the banks for the recent Sub-Prime Crisis. The blame should be placed on Community Reinvestment Act of 1995 (government social engineering). This agenda was not inflationary, but like that which resulted in ‘The Great Depression’, it was government mandated underwriting rules which resulted in the Sub-Prime Crisis. The similarities to the government sponsored lending which caused the collapse of banks in the 1920s been made by some referring to the Sub-Prime Crisis as the ‘The Great Recession’. We fail to see the impact of our own actions and blame our financial institutions. We have placed numerous regulations on Single-Family Home mortgage lending. Doing so gives us a slow Single-Family Housing sector and an excessively priced rental market. Many decry the lack of individual wealth creation in this economy. This is the direct outcome when we stymy home buying which has been the historical wealth-builder for individuals. Bank lending to businesses vs. individuals is far more skewed today than in the past. The actions of government have changed economic outcomes.

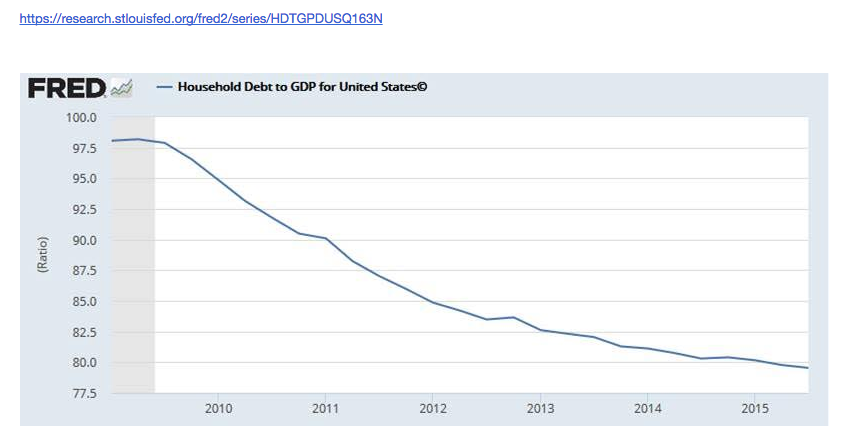

The end result of increased Single-Family Home mortgage regulation is an economy without the historic pace of Single-Family Home building. Single-Family Home building is running at roughly half the level historically. The Single-Family Home sector represents individuals spending 20yrs+ of future income in the current cycle. Individuals spend several hundred thousand dollars with the stroke of a pen and agree to pay it back with a mortgage. The impact during our historical economic upcycle has been significant. Today’s economy is slower because home mortgage lending is well under historical experience. At the current pace of ~3%, the Real Private Economy shows little of the excess which has led to past corrections. In fact,Household Debt to (as a Percentage of) GDP shows net debt lower relative to personal incomes. Financial risk to individual consumption is falling not rising.

It appears we will need a period of economic growth of several years near ~5% (~2% above the historical Real Private Economy trend line) before excesses build to a point from which a correction is likely to occur. Nothing like this is in sight for us. We do have a disparity with current bank lending skewed strongly against Single-Family Home ownership. It is likely that once calls by individuals, banks and home-builders are loud enough to be heard by their representatives, the lending regulations will change. When that point arrives, we are likely to see the economic excess we are not seeing today.

Macro-Momentum Investor calls for an economic correction is not supported by the current pace of the current cycle. In my opinion investors should remain optimistic for higher equity markets.