Last month the media said rising rates were going to cause a recession. This month rates are falling and they say that is predicting a recession. No wonder people are confused and worried. Which is it? Neither…..

“Davidson” submits:

Most investors and the media believe that price trends carry non-public and secret information about our economic future. This segment of investors are properly called “Momentum Investors”. They have very strong opinions which swing with every change in trend. This makes for great media content which is dependent on capturing consumer attention by providing a new point of view daily. For investors seeking to benefit from economic growth, the rapid shift in advice presented recommends active trading on information which at first appears optimistic, then turns rapidly pessimist only to turn optimistic again within a few weeks, often shorter. They provide this advice with such authority and seriousness that one feels compelled to act. This is emotional investing which has a long history of failure, but it sells a lot of advertising for the media.

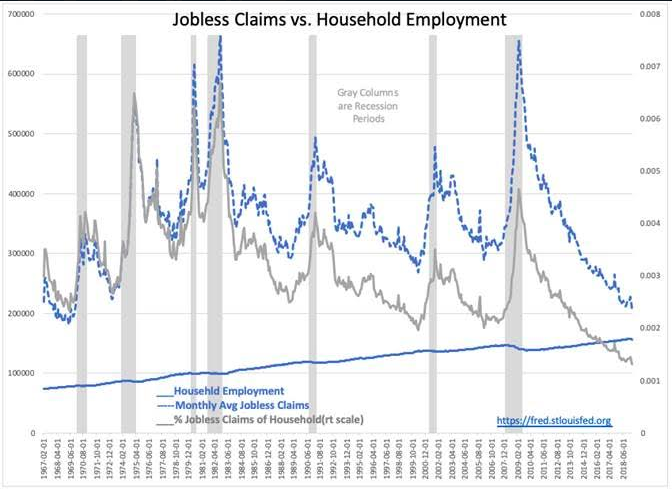

The past 18mos investors have been subject to rapidly shifting prices and multiple calls to sell everything to avoid being caught in the next recession induced downdraft. The economic data tell a very different story. The Jobless Claims vs. Household Employment comparison since Feb 1967 is one of the longest and most reliable of indicators because the pace of economic activity is organically connected to labor demand. Everything we measure in our desire to understand economic trends and whether we should invest in equities is based on labor demand. Real Private GDP, Real Personal Income, Real Retail Sales and on and on all are dependent on labor demand. The weekly Jobless Claims provide real time data to gain insight to labor demand with or without comparison to a broad employment data. Making the comparison simply provides additional insight.

The % Jobless Claims vs Household Employment always has turned higher at least 6mos and as much as 18mos prior to economic peaks and peaks in the SP500. That Jobless Claims continue to trend lower indicates that no recession is in sight and that economic expansion should continue. The SP500 from Feb 1967 compared with the 10yr/T-Bill Rate Spread helps explain confusing signals on which the current reliance on computer driven algorithms rely. Historically, the US market has corrected whenever the 10yr/T-Bill Rate Spread fell below 0.2% (RED ARROWS). The spread today is negative, -.05%. Why this no longer carries the signal of a slowdown in economic activity is defined by the current strong trend of labor demand and other economic measures.

One must step back and view the US market globally which has become a safe-haven for global capital in a world in significant transition. The last 20yrs has witnessed the monetization of assets in developing markets with the hope of spreading Democratic principles. One of the unexpected consequences has been the shift of this capital out of autocratic/Socialistic government controls to the US as business owners sought to improve their capital returns away from their deteriorating currencies. One can see that the pace of transfer into US$ based-assets has accelerated as REIT dividends and 10yr Treasury debt yields fell to historical lows. This has made the historical signal of the 10yr/T-Bill rate spread collapse as the current administration seeks better global tariff terms and pushes back against un-Democratic forces. Computer algorithms have been programed with historical patterns and can not take into account changing cultural norms or administrative policy. Algorithms have programmed narrowing rate spreads to previous periods of economic slowing and more recently have coupled this pattern to falling oil prices. This produces market turmoil in sharp contrast to current economic data which remains strong.

The recent trends in US GDP have accelerated with the Jobless Claims, Real Personal Income, Real Retail Sales and etc. continuing to signal economic expansion. These are hard counts of economic activity as compared to price trends which reflect temporary market psychology. Economic measures remain decent with no recession in sight!

To access member content FREE for 5 days, follow this link.