“Davidson” submits:

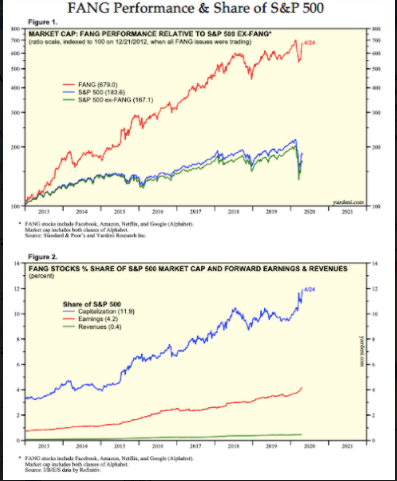

Every cycle has had its share of ‘high growth’ Momentum Investor driven issues which come to dominate the overall pricing of indices. This cycle is no different. The acronym “FANG”, created in the current market cycle, represents Facebook, Amazon, Netflix and Google. Yardeni publishes the disparity of performance vs fundamental valuation monthly. The latest chart shows that FANG issues have recovered nearly back to previous highs while the SP500 representing the 500 largest companies has not. 10 issues out of 500 comprise 23% of the market capitalization of the SP500 and are responsible for current outperformance carrying revenue and earning’s pricing well above the other 490 issues. Valuations are so elevated that most investors avoid these issues but not Momentum Investors, who investing with price-trends, have continued to pour additional capital into these favorite issues completely ignoring extreme valuation levels vs fundamentals. This produces a faster recovery for the index dominated by FANG-type issues than seen in managed accounts and most individual issues causing many investors to abandon sound investment approaches and chase performance. As investors chase performance, many well-managed companies lag behind indices till markets suddenly begins to pay attention.

Less experienced investors are always frustrated that their carefully selected funds or individual investments fail to keep up with FANG issues or even the SP500. The issue every cycle is that fear of losing business forces many portfolio managers to sell very sound companies and buy Momentum Issues because many investors are never sophisticated enough to think past quarter-to-quarter returns. This leaves many quality issues out of favor and discounted to historical valuations as Momentum Investing comes to dominate pricing. History shows that valuations eventually return to these companies but investors often become frustrated and chase performance of Momentum Issues just as issues long ignored come back into favor.

https://www.yardeni.com/pub/yardenifangoverview.pd

Many well-managed issues have been deeply discounted. The best recommendation is to buy these companies especially where insider buying has accelerated. Some of these issues are seeing insider accumulation at levels last seen in 2008-2009’s ‘Great Recession’. Corporate insiders are deemed the best informed Value Investors. This is why including insider buys/sales as part of one’s investment analysis is so useful. None of the FANG issues has insider buying which is typical of issues recognized as over-valued.

Buy equities, but be selective.