“Boring” is almost always better long term

“Davidson” submits:

The media touts the leading edge and untested ‘growth issues’ leaving little face-time for ‘value issues’. Newness is always exciting. News items emerge so frequently that the media is in a constant scramble to keep up with developments. It provides a heady mix for attracting viewership and advertising dollars. COVID unfortunately fell into this package, but it led to wall-to-wall coverage with massive advertising by pharmaceutical companies. The subsequent surges in revenue growth justified many new and even some existing companies falling into the ‘growth issue’ category. Now that we are post-COVID, the growth of ‘growth issues’ is not so much. Despite disappointing reports, ‘growth issues’ remain the focus of the media and most investors anticipating higher than normal returns. With a short-term focus, few recognize some well-established long-term investment basics.

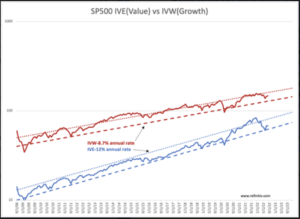

There is a mantra backed by many market studies over many market cycles. Tweedy Browne used to compile these studies a copy of which resides on Columbia University’s site. https://www8.gsb.columbia.edu/sites/valueinvesting/files/files/what_has_worked_all.pdfWhile every market cycle has many enamored of so called emerging ‘growth issues’, the record supports ‘value issues’ as the better option over time. SP500 IVE(Value)… shows that in the current cycle ‘value’ remains in the lead. This is likely to remain so forever and requires an explanation as it seems so misunderstood.

The reason why ‘value’ produces better returns than ‘growth’ lays in market dynamics of market psychology. Once this is understood, it will be an epiphany for most. The issues comprising each category are not static. Based on the criteria of revenue and price momentum, many untested companies are identified as ‘growth’ only to disappoint in delivering bottom line profitability. Many new issues after a few years simply crash and burn never to resurrect again as the concept could not sustain the scrutiny of markets and a competitive environment. Share price momentum on which everyone focuses, is one of the primary determinants of placing these issues in the ‘growth’ category and into the IVW ETF. Failure of untested issues is the reason IVW underperforms IVE. PayPal(PYPL) was a prominent growth issues in IVW. It has has survived and prospered while many failed to achieve their promise. Nonetheless, once it falls out of market favor and the criteria for ‘growth’, the categorization process places it in the ‘value’ group. PYPL in the most recent reconstitution has partially transferred to IVE. IVE now has PYPL as a 0.28% position vs 0.34% in IVW or ~45% Value vs ~55% Growth. Current pricing represents a 70% decline($310shr to $94shr) on a company well-operated since inception in 1998 and its IPO in 2002 but never priced as cheaply as it is today relative to its financials. Should PYPL’s management continue to grow PYPL as the CEO has forecasted, there should be a decent price recovery. On the current lower price, even a moderate repricing will contribute well above IVW’s 12% performance. To achieve ‘growth’ status again will be quite a task, but returns to investors who acquire PYPL at current levels should prove beneficial. Do this with every well-managed company that has fallen out of favor and one can build a portfolio of companies likely to outperform. It should be obvious that this is not a buy-hold approach as every recovered company will in all likelihood become over-priced once again. One must monitor each position for its own financial and pricing metrics and make decisions within the context of the market environment as it develops. In summary, that ‘value outperforms ‘growth’ comes from the dynamics of issues being assigned by pricing criteria to each category.

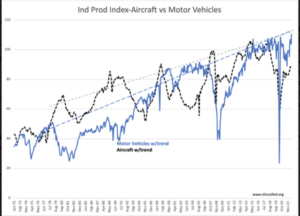

Note that IVE remains near its channel trend lows. PYPL is one of the issues to which one should pay attention in my experience. Others well outside most investor’s focus are companies involved in manufacturing aircraft and vehicles. The demand for new vehicles and aircraft is strong. Having a 2 ½ period of almost no supply, one can expect a multi-year period of production to meet global demand which has only continued to grow. The most recent Ind Prod indices for these sectors demonstrate a sharp recovery is underway post-COVID. Aircraft and vehicle manufacturing related issues populate IVE and investing in those which are well-managed and most heavily discounted one should achieve decent returns.

‘Value’ always outperforms ‘Growth’. How one makes investment selections must always include an analysis of market dynamics.