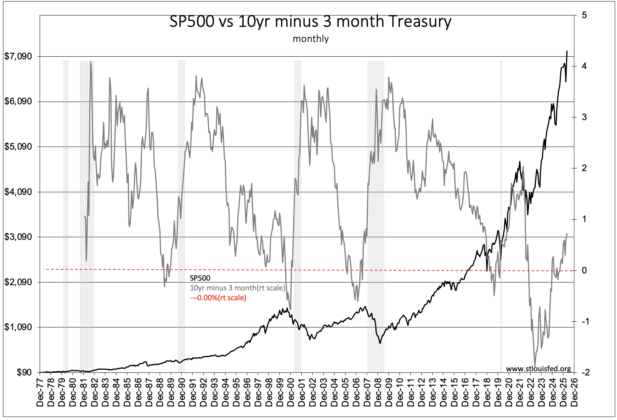

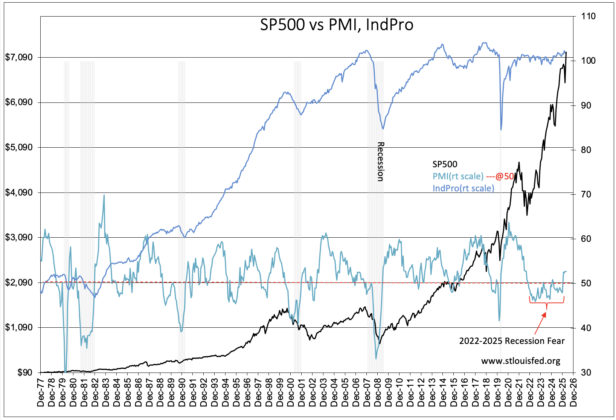

The Manufacturing PMI for April holds at March levels. In addition, the 10yr minus 3mo Treasury spread has widened to 0.72% for which there is long-term interpretation of debt capital shifting into equity capital. The shift into positive territory for the 10yr minus 3mo Treasury had a brief excursion in 2024 but then retreated till the current run broke above 0.0% in Sept 2025. It certainly appears that the moves in the PMI and the 10yr minus 3mo Treasury are correlated. Both, are market psychology indicators as is the SP500.