We’ve addressed our feelings on the uselessness of CAPE before but I am seeing it being used frequently once again so it is time to revisit….

In fact, the WSJ just referred to it again…..CAPE hasn’t “worked” in over a decade at predicting anything (not that it ever really did)…it.s time to put it to bed

“Davidson” submits:

CAPE has an issue which misses a significant market perception. The issue is earnings are adjusted for inflation which causes the CAPE ratio to rise over time. The market already makes an adjustment for inflation and is why market P/E ratios have a long term range that is about the same for the past 70yrs. That range is 7-8 at lows during heavy inflation to about 20-25 at market peaks.

The better method for market pricing is to apply Knut Wicksell’s ‘Natural Rate’. To do so one uses the long-term trend of the Real Private GDP. Data available from 1949. It has gradually drifted lower as the US economy has risen from ~3.9% to ~3% today. This is the US fundamental growth rate as a Democratic society under the rules which we adjust fairly often as we seek better self-governance. Add to this an inflation measure. I use the 12mo Trimmed Mean PCE produced by the Dallas Fed to produce a measure of the ‘Natural Rate’. Today the rate is ~4.7%

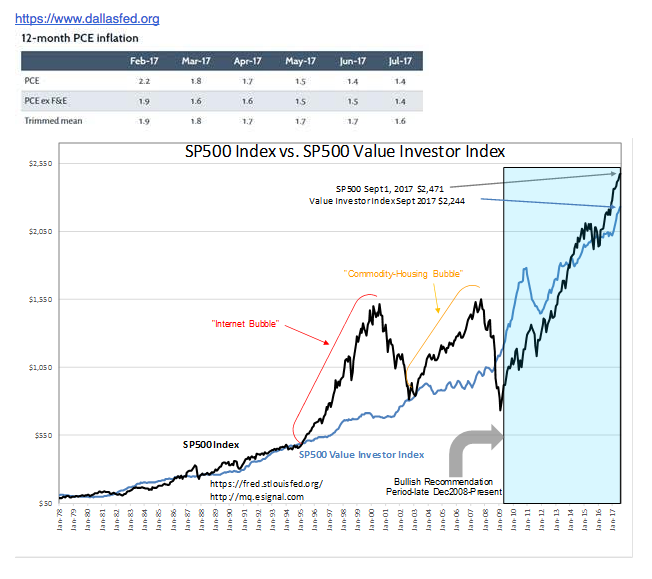

The ‘Natural Rate’ is a fundamental capitalization rate. This is applied to the long-term earnings trend for the SP500 to get a price justified by this rate. The result I call the Value Investor Index. This index tracks major market lows. It represents how Value Investors view opportunities in the SP500. Their buying is most active at market lows which is why markets find support relative to fundamentals as Value Investors seek opportunities. Momentum Investors make no such connection. They fear ‘market failure’ as Value Investors only see the lows of a market cycle.

The 12mo Trimmed Mean PCE inception date is 1978. The chart of the SP500 with The Value Investor Index is below. The issue with CAPE is that:

1) Value Investors already adjust valuations for inflation when they seek opportunities. Higher inflation = lower P/Es.

2) this relationship only works for market lows-not for pricing through the entire cycle.

There is no formula for prices which can hold for market bottoms and peaks. The investors are different. Value Investors buy on fundamentals while Momentum Investors buy on price-trends and media headlines well after fundamentals are known. Value Investors create major recession lows. Momentum Investors create cycle peaks. The dominance of investor influence changes as the economic/market cycle evolves. There is not a consistent relationship for the entire cycle. The CAPE misses this market dynamic as well.

Markets at the moment are only 10% above the Value Investor Index. While this index does not have a specific level at major peaks, history shows that something more in the range of 50%-100% premium is more likely than the current 10% premium. There is another indicator which is very reliable to identify speculation levels and market cycle peaks. More on that if this interests you.